One of the longest-running problems in the Bitcoin ecosystem for businesses has been banking relationships. Prior to NYDIG and their recent efforts to start plugging American banks and credit unions into Bitcoin rails, the only banking options for businesses in the space were Signature Bank in New York and Silvergate out of California. Major banks have been very combative and at odds with businesses in the space for years. Hell, they've been combative and at odds with their own customers simply trying to patronize Bitcoin businesses, closing accounts or shutting down cards for years now at this point. No businesses have exemplified the hostile and antagonistic nature of these interactions more than Bitfinex and Tether. Not just in the case of banks either, but legacy regulators.

One of the first big instances of Bitfinex running afoul of this antagonism was in 2016. The Commodity Futures Trading Commission ordered them to pay a fine of $75 thousand dollars for failing to register as a futures commission merchant (FCM) under the Commodity Exchange Act (CEA). This was ultimately the result of Americans trading leveraged financial products on the platform without Bitfinex complying with the appropriate regulations. The key point of the regulation revolved around what constituted actual delivery of the underlying commodity and in what time frame it occurred. In order to escape registration requirements you are required to be able to prove actual physical delivery of the commodity (bitcoin) within 28 days. Because all of the Bitcoin backing the leveraged products were custodied by Bitfinex and only credited to users accounts, this was viewed as not meeting the definition of physical delivery, and therefore Bitfinex was required to register as a FCM.

To sidestep this registration requirement Bitfinex ended up contracting with Bitgo to restructure how their bitcoin storage system worked in order to comply with the regulation's requirement to physically deliver within 28 days. They provided each user a segregated multisig wallet which Bitgo co-signed for and began storing each individual user's funds in separate wallets. This would be the first in a long line of events that can be ultimately described as antagonism from regulators and financial institutions forcing a business in this space to either comply with burdensome regulation or engage in riskier behavior in order to circumvent the need to comply. Ultimately this architecture change is what allowed a still unknown entity to compromise their system and get away with 119,756 BTC. Had this system not been implemented, I remind you specifically to comply with U.S. regulations, then only a tiny fraction of those funds would have been available in a hot wallet that could be remotely compromised. Even though you could put some of the blame on Bitfinex for not registering as an FCM, the regulations even putting them in the position where they had to comply or be compatible with a loophole is ultimately what created this situation in the first place.

This is a pattern that repeats itself through the entire history of Tether and Bitfinex in this ecosystem. Whether it is direct pressure from the regulators themselves, or indirect pressure in the form of regulated entities cutting business ties with Tether or Bitfinex, the story of both companies is the story of being pushed further and further into a corner as they were methodically and progressively ostracized by jurisdictional regulators and financial institutions from the United States.

Tether was originally created in 2014. For a short period it was known as "Realcoin," but after a month everything was renamed to Tether. The company and product were founded by Brock Pierce, Reeve Collins, and Craig Sellars. The initial launch of the company involved three different stablecoin tokens being issued: one for the U.S. dollar, one for the euro, and lastly one for the Japanese yen. All of these tokens were issued and circulated directly on the Bitcoin blockchain using the protocol Mastercoin (later rebranded to Omni).Omni is a second-layer protocol on top of Bitcoin using OP_RETURN to record the issuance and transfer of new tokens inside of bitcoin transactions without requiring the Bitcoin network to enable new rules (everyone who cared about the tokens could validate new rules around them and refuse to accept invalid token transactions, while everyone else could just ignore new rules and see "gibberish" encoded on the blockchain).

The reason for wanting to do this in the first place is sort of in a way the reason for Bitcoin existing in the first place, i.e., you want all the benefits Bitcoin provides minus the volatility. You want Bitcoin plus stability, i.e., a stablecoin. Bitcoin is a mechanism that allows things to settle with finality in ten minutes (and nowadays with the Lightning Network instantly), but the bitcoin asset is very volatile. So putting a token on the blockchain backed by fiat in the bank brings that same settlement efficiency (as long as you trust the people holding the fiat in the bank) to more stable fiat currencies. Now given the antagonistic way banks have dealt with companies in this space, the utility of this should be pretty intuitive. Instead of having to deal with all the problems of banks refusing transactions and wires, or specific relationships between transacting parties, you just have to get the money into a bank and can transact with the token on the blockchain. All of those annoying fiat bank problems can be pushed to the time of final redemption of the token for real bank money instead of having to be dealt with every time you make a single transaction.

Given Bitfinex's situation in hindsight it shouldn't surprise anyone they enabled trading of Tether at the start of 2015 a few months after the company and token’s launch. The ability to delay actual bank settlement in transferring fiat balances is a natural alleviation if your problem is friction dealing with the banking system. For a few years this arrangement worked very well, even to the point that other exchanges who also had troubles with the banking system used Tether for access to fiat liquidity in operating their own businesses, but eventually the legacy system began to ostracize Tether. In early 2017 Wells Fargo began blocking payments to and from Tether that flowed through them. They were the correspondent banking partner with the Taiwanese banks that Tether (and Bitfinex) were using to custody fiat funds. Both companies filed a lawsuit against Wells Fargo, but within a week both suits were dropped.

This led to a year or slightly more of banks playing whack-a-mole with Tether and Bitfinex. Right after the Wells Fargo wire blockage, Bitfinex also had all banking relationships severed by their Taiwanese banks. During this time period both companies bounced around through multiple banking relationships. Things got to the point where new accounts, sometimes even under newly incorporated entities, were being opened up in a shell game of trying to move money in and out and keep it shuffling around before any bank realized the deposits were for cryptocurrency activity.

August in 2017 marked the start of a new phase for the avalanche of attention from banks and regulators in the United States. Twitter user Bitfinex’ed (@Bitfinexed) made his first accusation against Bitfinex and Tether for systemic market manipulation of the entire ecosystem. His post went into defining a supposed trader on Bitfinex he called "Spoofy," and his accusations that Spoofy was engaged in widespread market manipulation on the platform. For those not familiar with trading, spoofing is a practice of putting orders in on an exchange to buy or sell something and then removing the orders when the market price reaches the point things would actually be bought or sold. Lots of the time other traders will front run and start buying or selling before those orders would be hit, so a trader with enough funds can actually push the market price around by effectively tricking other people into buying or selling, and then removing their own orders without having to fulfill them. Bitfinexed's accusations were that this behavior could very well be Bitfinex themselves, and that the behavior was a systematic manipulation of the entire crypto market. He later went on to outright accuse Tether of printing money out of thin air with no backing, but in this initial post he left it insinuated instead of accusing them outright.

For the next year or so Tether was constantly berated by accusations of fraud, market manipulation, and not being fully backed by dollar reserves. They contracted with Friedman LLP to conduct an audit of Tether reserves, but all that was ever published by the firm before Tether severed the relationship was attestations. The difference between an audit and attestation is an audit would comprehensively look through an entity's balance sheets including assets, obligations, revenue, etc., to build a comprehensive picture of how those all balance out, where as the attestations simply attested to witnessing proof of holding certain assets or currency in reserve at the time of the attestation. Eventually the relationship ended due to, paraphrasing Tether's statement on the matter, "the large amount of time and resources being spent on the very simple Tether balance sheet meaning the audit will not be produced in a short enough time frame." I would like to point out here though, unless this has recently changed in the last year or two, no other stablecoin I am aware of has published an actual full audit of their operations. So the framing back then in the context at the time I feel was a completely disingenuous singling out of Tether and demanding a higher standard of transparency than what was demanded of other stablecoin issuers.

Throughout this whole saga in late 2017/early 2018 both Bitfinex and Tether completely cut ties with U.S. customers. Two other important factors in this story occurred around the same time period, although they were to differing degrees not publicly known until later. One was Tether and Bitfinex beginning a banking relationship with Noble Bank in Puerto Rico, a 100% reserve bank founded by Brock Pierce (an original founder of Tether), and the other was Bitfinex beginning to utilize Crypto Capital for fiat payment processing. This was the entity constantly shuffling money between new bank accounts set up under new corporate entities.

Before getting into the unraveling of one of these stories (regarding the Noble Bank relationship) it's worth mentioning a short period of time in early 2018 when Bitfinex had a banking relationship with Dutch bank ING. I mean very short. Within a few weeks of Bitfinex publicly acknowledging the relationship, ING closed their banking accounts. Later in 2018 Tether and Bitfinex severed ties with Noble Bank, and the bank was put up for sale. The publicly-given reason was the bank’s lack of profitability as a full reserve bank, but my own speculation is that their own custodial bank New York Mellon was likely pressured by New York regulators to in turn pressure Noble Bank for their relationship with Tether and Bitfinex. See the continuing theme? Banks and regulators constantly ostracizing both companies from banking services is the pattern here. After jumping ship from Noble, Tether began holding reserves with Deltec Bank in the Bahamas.

Now here is where the story gets absurd. In 2019, $850 million dollars of Bitfinex funds held by Crypto Capital were seized by multiple governments, one of which was the United States. The company had been opening bank accounts under shell corporations and claiming to the banks that they were engaged in real estate transactions in order to process deposits and withdrawals on behalf of Bitfinex, Tether, and other cryptocurrency companies using their services. For months the company led Bitfinex on, would not fully explain the issue, and eventually Bitfinex addressed the problem by taking a loan from Tether out of their backing reserves. This is when the New York Attorney General sued Bitfinex and Tether for being short $850 million in Tether reserves. The United States government seized almost a billion dollars, and then sued the companies the money was stolen from for not having that money.

This case dragged on for almost two years until February 2021, when Tether settled with the NYAG for an $18.5 million dollar fine. They were required under the terms of the settlement to issue quarterly reports of exactly what was backing Tether.

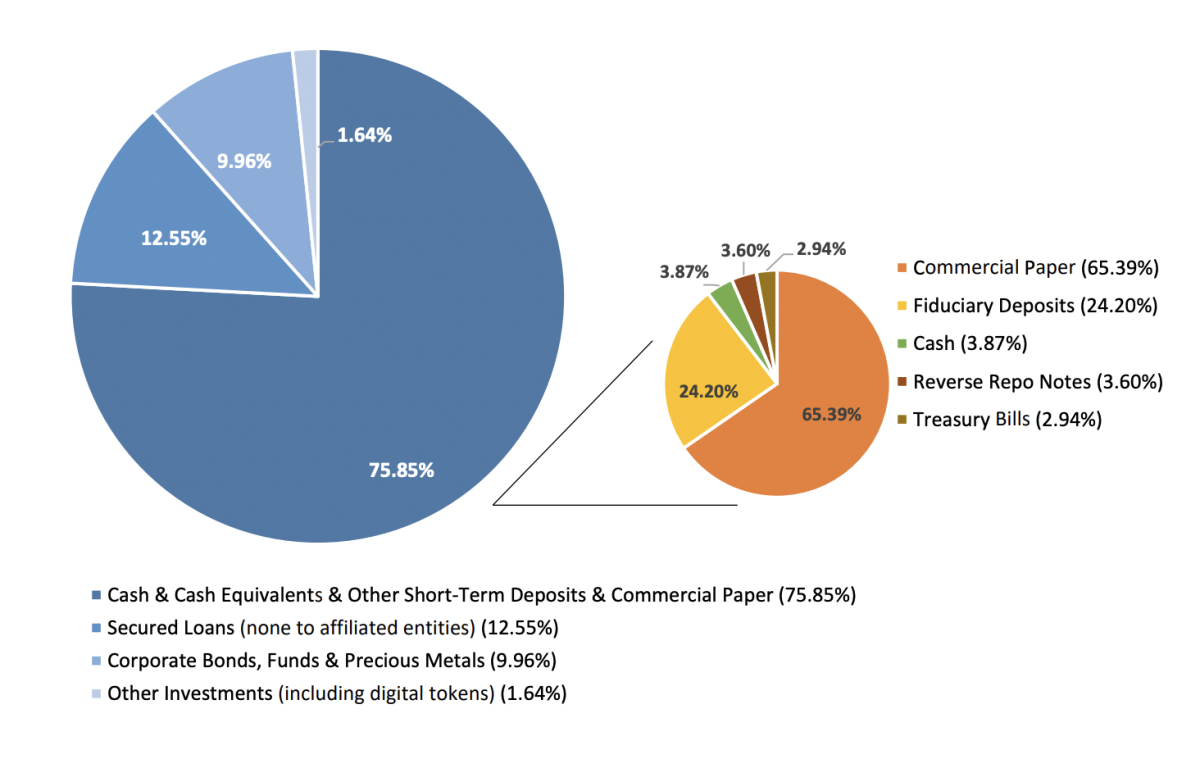

Only about 6% is real cash reserves or treasuries under Tether's direct control (for clarification to readers not familiar with such details, "fiduciary deposits" are effectively bank deposits not directly held by Tether). The balance sheet of reserves is essentially the inverse of what it started as. In the beginning Tether actually did have hard cash on hand for reserves, now the majority of their reserves are simply commercial paper (short-term loans issued by corporations). The risk profile of this versus simply holding physical cash is massive, as the value of all that commercial paper is effectively only as stable as the company that issued it.

That said, why are they in this position in the first place? Because of the years of regulators and banks constantly cutting them off from fiat financial rails and pushing them further and further into a corner. Think about that for a minute. The entire chain of events that led to a much riskier balance sheet profile, which puts anyone holding Tether at a greater risk of losing their value, was caused directly by constant antagonism from banks and regulators. It doesn't change the risk, but I think it is an important context to provide.

So what lies ahead for Tether?

Given the recently announced El Salvadorian Bitcoin bond, and the fact that Bitfinex will act as the broker and Tether will be accepted as payment, I think the road ahead for Tether is going to be very dangerous in a sense. Simply existing as an alternative fiat settlement system has led to non-stop harassment and scrutiny from governments and banks that have at times pushed both businesses to the point of potential failure and liquidity crises. That was just for passing dollars around between exchanges. They are now, after having already been backed into a corner, literally facilitating the sale of the first sovereign Bitcoin bond in human history. If just moving money between crypto exchanges has elicited the level of regulator and bank ire that Tether and Bitfinex have been subjected to, what will this bond issuance elicit?

I fully believe in response to this, the United States government will be coming for both Bitfinex and Tether in full force. The setting of the stage for that is written all over their recent obsession with stablecoin regulations, USDC's recent move in response to this wind change of shifting all reserves to short-term treasuries, and in general the entire historical response and antagonism of both companies. The United States has subtly reacted to this ecosystem existing the way an immune system reacts to a virus, and with things evolving to the point of a nation-state issuing a bond backed by bitcoin, that immune response will likely increase.

I have always considered the attacks, and frankly deranged conspiracy theories, surrounding Tether are absurd. But that doesn't change the fact that attacks against them have continued increasing in intensity while they have been backed further and further into the corner. The more that Tether, and by proxy Bitfinex, facilitate the evolution of this ecosystem financially beyond the control of the existing U.S.-dominated financial system, the more the hammer will be swung at them. Just because prior whacks have missed doesn't mean all attempts in the future will. To think so is to subject yourself to the gambler's fallacy. Not to mention the basket of issues commercial paper backing introduces in terms of stability risk tied to general global financial markets, i.e., if the companies who issued that paper do poorly, become insolvent, or can't make good on the paper then there are no dollars backing that Tether when any of those things happen. That becomes the rock to the government antagonism's hard place. On one side the traditional banking system and regulators squeezing them into a corner, and on the other the risk of economic misfortune of issuers of the commercial paper effectively deleting that Tether backing if defaulted on.

And to top all of this off, very recently the rebel government of Myanmar in their fight against the military government adopted Tether as a currency.

What do you think the domino effects of that will be? I think they will result in Tether being backed further into a corner, and more frantic swings of the hammer will come. Maybe this is me being a pessimist, but I have always thought if Tether came to an end it would be due to the U.S. government having enough of it. I think they're about at that point.

This is a guest post by Shinobi. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.