This is an opinion editorial by Joakim Book, a Research Fellow at the American Institute for Economic Research, and writer on all things money and financial history.

All (fiat) monies struggle with getting their users to hold the liabilities of their issuer. Put differently, only issuers with some degree of trust or credibility manage to “monetize” some part of their debts, by literally having others carry it for them for free. In the extreme, it means that the issuer gets a perpetual, non-redeemable, interest-free loan with which it can finance a portfolio of assets — the profits of which they may spend as it pleases. The most well-known instance of this is the Federal Reserve Board, and its seigniorage profits are remitted back to the U.S. Treasury.

Commercial banks do this too, but on a lower layer in the monetary hierarchy. When you’re depositing Fed notes at a commercial bank, you’re giving up a higher-level fiat liability for a lower-level bank deposit — and you’re financing the bank’s portfolio, these days usually earning interest rates of zero.

In the past, commercial banks would issue private bank notes (non-interest-bearing liabilities) that could only stay in circulation if its clients decided to hold them, which they only did if they found some convenience in doing so. British banks of the 1700s and 1800s, for instance, offered highly decorative notes, proudly displayed their balance sheets and bragged about their conservative lending standards, deep-pocketed owners and other reasons for clients to trust that their hard money was safe. Banks competed for note-issuing business, since notes kept in circulation meant interest-free financing of its assets.

A few steps down in the modern debt-based fiat monetary hierarchy we find a company like Starbucks. While not a bank, it still issues money — although debt-money of a peculiar kind. Starbucks have dollar-values stored in outstanding gift cards: value that consumers have essentially lent to the company at zero percent interest. About 6% of the company’s outstanding liabilities are in this form, redeemable and repayable not in dollars but in coffee (which lets it avoid banking licenses or regulations for money transmitters). For promises of future coffee and/or loyalty rewards, customers are willing to give Starbucks their dollars up front.

All of this is to show that swaying customers to hold your liability is the secret to monetary superpowers.

All Monies Have Value Because You Hold Them

While all cryptocurrencies are outside money rather than inside money as the trad-fi entities discussed above (i.e., they are assets, owned outright, outside the banking system, rather than debt claims on a bank-like entity inside that system), they struggle with a similar problem of acquiring liquidity. For your “crypto” project to be successful, you need to somehow sway clients into holding its tokens — to hand over valuable financial resources in exchange for a stake in its cryptocurrency.

As the most mature and secure cryptocurrency, bitcoin has a major (and uniquely distinguishing) advantage over every other cryptocurrency: it doesn’t have leaders in control of the money supply, known founders or venture capitalist backers, pre-mines or any other feature that makes cryptocurrencies more like financial securities than the pure monetary asset that is bitcoin. People want to hold bitcoin for its use as (future) money, and not for any loyalty reward or promise of yield or scammy pump-and-dump promise of future glory.

Every single shitcoin, ETH included, fights over available liquidity, and must therefore come up with schemes and reasons to make their users hold their (worthless) token. See all the “staking” practices around, where nifty “crypto” projects tap into illusions of “yield”: if you hold the token today, we’ll pay you more of that token in the future (never mind the dilution and price change, lol!). Dreaming of untold riches, venture capitalists ape in and the hope is that their funding lets projects continue long enough that millions of users have acquired an organic(-ish) money demand.

To engineer money demand, most shitcoin issuers literally bribe their users with newly created or previously minted tokens — digital funny money with no purpose whatsoever. Incentivizing people to part with real-world value for fake-world shitcoins is the only way they can bootstrap their worthless digital plaything into some kind of value. Fool enough people, for long enough, and you can engineer your way into a stable, continually rolling-over money demand, interest-free liabilities or exciting seigniorage (cue Tether).

Matt Levine at Bloomberg writes:

“Much of crypto economics consists of some version of ‘if you assume this thing is valuable, then it is valuable.’ That is true in some loose sense of lots of other investments, too, but crypto has really managed it at scale.”

He extends that take to “algorithmic stablecoins,” stablecoins that aren’t backed by (a semblance of) reserves, like commercial banks of the free-banking past, but relying on trading arbitrage between two cryptos that the project controls:

“The way you dress it up will generally be with some sort of Ponzi-ing, because that is the main way for self-contained crypto projects to create value these days. You say ‘hey if you deposit dollarcoins we’ll pay you a 20% yield in sharecoins,’ or ‘if you stake sharecoins we’ll give you a 20% yield in sharecoins,’ or whatever, and the interest rate on this — the rate at which people are given new sharecoins created out of thin air — is high enough that people get excited and do it for a trade, even if they understand that it’s all made up."

The result is that “You Ponzi your way to widespread acceptance, and then you maintain the value mostly through the widespread acceptance, not through the algorithmic peg mechanism.” Which, incidentally, isn’t far from how governments persuaded (forced?) their citizens to accept worthless pieces of paper rather than commodity-backed money.

Without a way to replicate Bitcoin’s immaculate conception, proof-of-stake chains must compete for money issuance by persuading their users to part with valuable assets in exchange for promises of a larger share of a future shitcoin print.

In contrast, bitcoin bootstrapped its value from zero to something by users — freely and willingly and without faux promises or financial incentives to hold the token — using electricity and computer hardware to validate blocks and mine bitcoin into existence.

Russia’s Pretend Gold Standard And The Ruble As Just Another Shitcoin

Depending on who you’d believe, and whose faulty economic framework you follow, in recent weeks Russia has both established a gold standard and abolished it. Give it enough time, and I’m sure some clever-by-far economist will comment how this once again shows the impracticality of tying money to hard assets, like commodities.

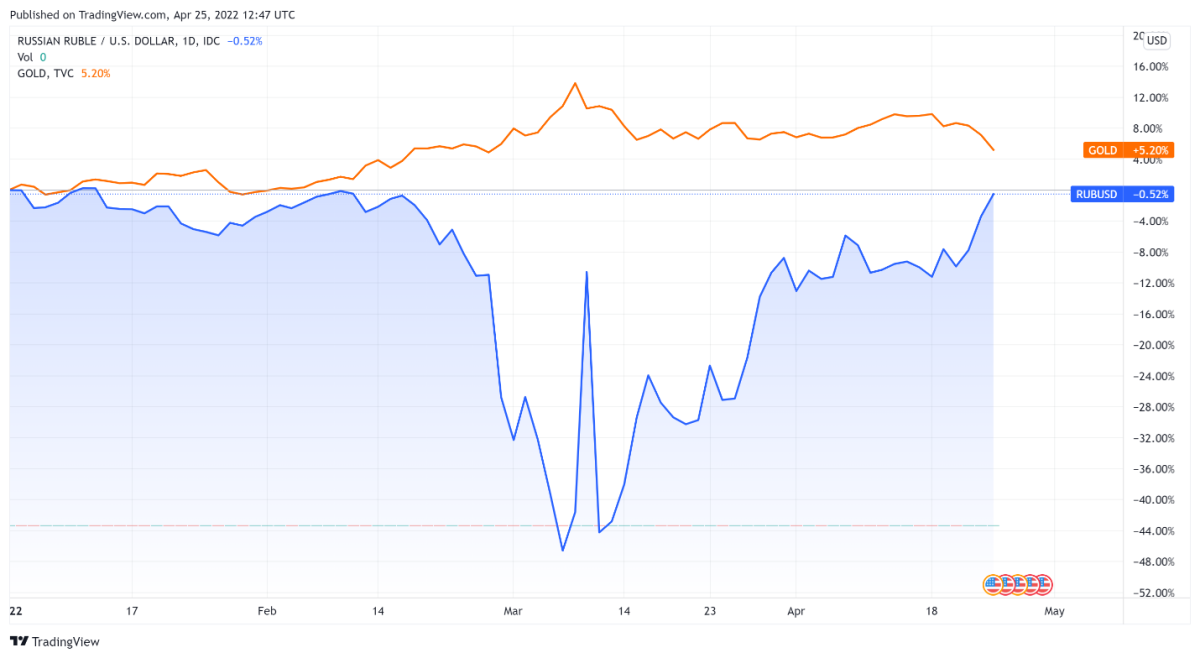

One day in late March, officials in Putin’s administration were not-so-credibly promising to buy gold at 5,000 rubles per ounce, which quickly made the ruble trade higher against other currencies (though with pretty restricted capital flows). A few weeks later, as Russia’s currency had strengthened enough to make 5,000 rubles a decent above-market price for gold, the central bank stopped its one-sided price-fixing of gold. Nothing to see here.

When a government promises to tie its currencies to some assets it doesn’t control (other countries’ currencies or commodities like gold), its monetary authority stands ready to buy and sell at given prices. If the financial market traders with which it interacts believe in them (credibility), or if the monetary authority has enough foreign reserve/hard-money assets in store, this policy of pegging one’s currency can be successful. If not, sooner or later speculative attacks take place, and the government is forced to correct their course. Markets, like physics, can be brutal.

Source: TradingView.

Since the gold announcement, the ruble has recovered the level it held against USD before the Ukraine invasion. Did the gold-backing stunt therefore work?

More likely, this was all a quick-fix credibility play, making the ruble somewhat more desirable for others to hold — if only briefly for transactional purposes. For The Financial Times, Robin Wigglesworth summarizes: “Imports have been crushed, interest rates have been doubled, harsh capital controls have been put in place, and Russia’s oil and gas sales means it continues to accumulate foreign earnings.” No wonder the ruble trades higher on a much smaller market.

Besides:

- Gold standards operate on trust: and nobody trusts Vladimir Putin, so it’s very unlikely that this would do much.

- The ruble-gold play still lacks the redeemability feature that makes for true outside money. Depositors of, say, BlockFi can redeem their BTC deposits into sats; depositors of, say, Bank of America, can withdraw bank money into outside-money cash notes. Holders of rubles can ... not do anything. Redeem them for gold …?

All currencies fight for liquidity and one tool they use in that fight is offering reasons for their users to hold their debt or token. In that sense, the plethora of shitcoins aren’t that different from the ruble, its issuer desperately trying to shore up fake demand and limit outflows from its monetary network. Levine again:

“... people mostly don’t trust the dollar because you can earn 100% interest on dollars, or even because you can earn a small amount of interest on dollars; they trust the dollar because they trust the dollar, in a circular, widespread-social-adoption sort of way. You don’t need to end up with a Ponzi scheme.”

It’s hard to tell where the ruble, freed of internal capital controls and foreign sanctions, would trade against the USD. And it’s hard to stipulate where fiat currencies would trade against hard assets like gold or bitcoin were they freed of government control and taxation.

The circularity of monetary demand is what all currencies aspire to, and the Central Bank of Russia has recently shown us some of the shitcoin tools it wields. The Russian currency may be one step up in respectability from shitcoinery, but it’s shitcoinery nonetheless. In contrast to many of its digital rivals, it has large supplies of commodities, natural gas and gold supplies that it can use to defend its token or engineer monetary demand for it — not to mention an army, a bureaucracy and a tax system.

The sociolinguist Max Weinreich is supposed to have quipped that “A language is a dialect with an army.”

We could say the same about shitcoins and fiat currencies.

This is a guest post by Joakim Book. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc. or Bitcoin Magazine.