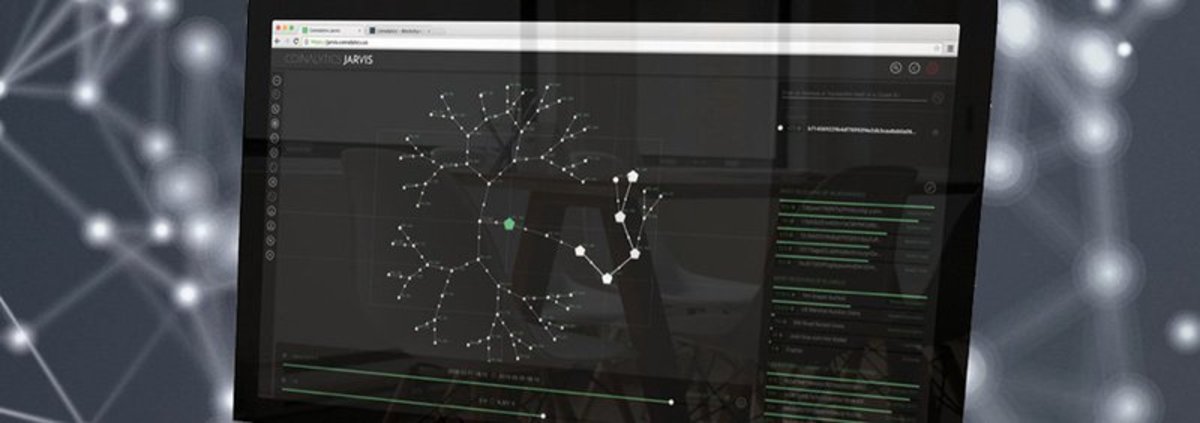

Analysis by Steven McKie.Big Data. It’s a popular buzzword that you've seen all over the Net the past few years. It’s a very serious billion-dollar industry now — with frontrunners from all different niche avenues of data collection and analytics. With the number of unique data sources available to these data-focused companies, the possibilities for analytics and selling that service to others seems exponential. And, with the rise of worldwide ledger-based systems like that of Bitcoin and other blockchain-based technologies, the lines are blurring between what's kosher in extrapolating data from the public domain and what isn’t.There are plenty of reasons to gather large amounts of information, especially in realtime. The ability to identify trends, track data from its source to its endpoint, and making inferred correlations between data points is highly sought after – especially the storing of that data for future analyses and historics, primarily in the business/financial world.But, what about the data on the most private things we do in our everyday lives? For instance, buying things online and in stores, filling prescriptions, sending money to friends. Surely there exist financial institutions and businesses that monitor that information for security/reporting purposes? And surely they report any suspicious activities to the appropriate authorities for matters of national security (see KYC/AML).Many regulations already exist that require this level of oversight for financial institutions, especially those in the United States. These data analytics help the government and other agencies have more oversight into a hyper-connected populous.Fair enough.But what about when all that information is already in the public domain, and not private? Bitcoin and its distributed public ledger system allows for the entirety of all transactions on the network a certain modicum of “pseudo-anonymity.” Every transaction you make on the network is publicly available, but your particular “wallet address” and identity is uniquely known only to you and whomever else you transact with – or the custodial wallet service you may be using, i.e. Circle or Bitreserve. But if you’re using a newly generated address from your personal home wallet to send funds, or using stealth addresses (learn more here), you are more masked from analytics-based systems that would seek to interpret and make inter-correlations in regard to your transactions.But who’s working on those types of systems? Bitcoin Magazine had a chance to speak with Bill Gleim, Co-founder of Coinalytics, who took the time to describe Coinalytic’s realtime analytics platform in his own words:“I realized, as an early victim of bitcoin thefts, there needed to be a better way to understand blockchain activity," he said. "My original motivation is a mental framework where participants justifiably trust the blockchain and other cryptoledgers with which they interact, particularly in terms of privacy and security.”What does “understand blockchain activity” mean, though? Gleim went on to explain his plans for the long-term:“We want to continue providing actionable insights for customers with widely-varying requirements," he said. "Currently, our data intelligence layer is focused on financial transactions on the Bitcoin blockchain, and we are excited to expand this data intelligence layer to areas like the Internet of Things and smart contracts in the future.”Hmm. Sounds, interesting, definitely. But, let’s go a bit deeper.One of the key components of Coinalytics is a system they are calling “Jarvis”. Jarvis, is described on the Coinalytics site as: “A visual and analytical workspace to perform in-depth investigations across the Bitcoin blockchain. Built on top of the Coinalytics back-end, the user interface allows you to visually interact with an enriched version of the blockchain and focus on transactions and entities of interest to analyze relationships and uncover hidden patterns.”Now it’s starting to make sense. Coinalytics plans to data-mine the Bitcoin blockchain in order to “uncover hidden patterns,” aka monetize the act of making sure you and businesses are not transacting with bad actors or known criminals. Or by helping larger financial institutions better adhere to differing regulations passed at a state and national level as they transition into adopting digital currencies such as bitcoin, blackcoin, and litecoin.This solution would ultimately allow banks to better trust the individuals they might be interacting with on the blockchain, or aid a governmental body tracking down a series of “bad” transactions to a particular e-criminal.To be fair, the data is, in fact, publicly open to interpretation. Surely someone was bound to come along and analyze it on an enterprise level. We asked Gleim specifically whether he planned to work with any governmental agencies with his platform.“Yes," he said. "We provide data intelligence software to all kinds of companies and organizations.”Surely there will be individuals who will be wary and suspicious of such a service, bad actors or not. However, people always find a way to circumvent potential privacy busters such as these.Luckily, with the current release of BlockStream’s open source project, “Sidechain Elements”; the ability to use bitcoin as anonymously as cash will still be possible via sidechains. As well as many other current services that seek to improve the anonymity of bitcoin transactions, such as Dark Wallet, coin mixers, etc. Rest assured, there will always be a solution cropping up that further protects your privacy; that's the power of open source.We asked Gleim what his personal views were on Bitcoin anonymity and services as whole.“As a proponent of personal privacy, I believe anonymity is desirable in many circumstances, and in other circumstances privacy, traceability and reputation are more important," he said. "I would like to see the market needs for Proof of Identity, Proof of Privacy and even Proof of Anonymity fulfilled by Bitcoin.”Gleim’s position as Technical Lead at Coinalytics is no surprise. He also has held positions at companies including Google, Motorola, and bitcoin alternative Ripple Labs. It’s great to see that someone who’s developed a system like Coinalytics/Jarvis also understands the importance of anonymity, and how that will play part in its growth, as businesses are built on providing services the blockchain itself cannot fulfill.The bitcoin transactional flow is shaping up to look like this: major financial institutions transacting openly and transparently via the public ledgers to be regulated accordingly in real-time. And individuals transacting publicly or anonymously via sidechains, stealth addresses or whatever anon-related service they’re privy to.This contrast is similar to that of current debit/credit card purchases and cash. You give up privacy for mainstream purchases with debit/credit card providers, and then anything private or sketchy can be done via cold, hard cash.The whole idea of Bitcoin becoming a global financial system is slowly starting to seem a lot more feasible.It’s great to see the services and systems built around the bitcoin blockchain mature and grow to not only work alongside regulators, but to also see other services/systems emerging to equally subvert them at the same time. And, for those gripping to the eternal libertarian roots of Bitcoin, this is not a fond farewell to the anti-government/privacy-centric ethos you all know and love. This is just a technological compromise.For now. Images courtesy of Coinalytics.co