The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine's premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Options And Derivatives Update

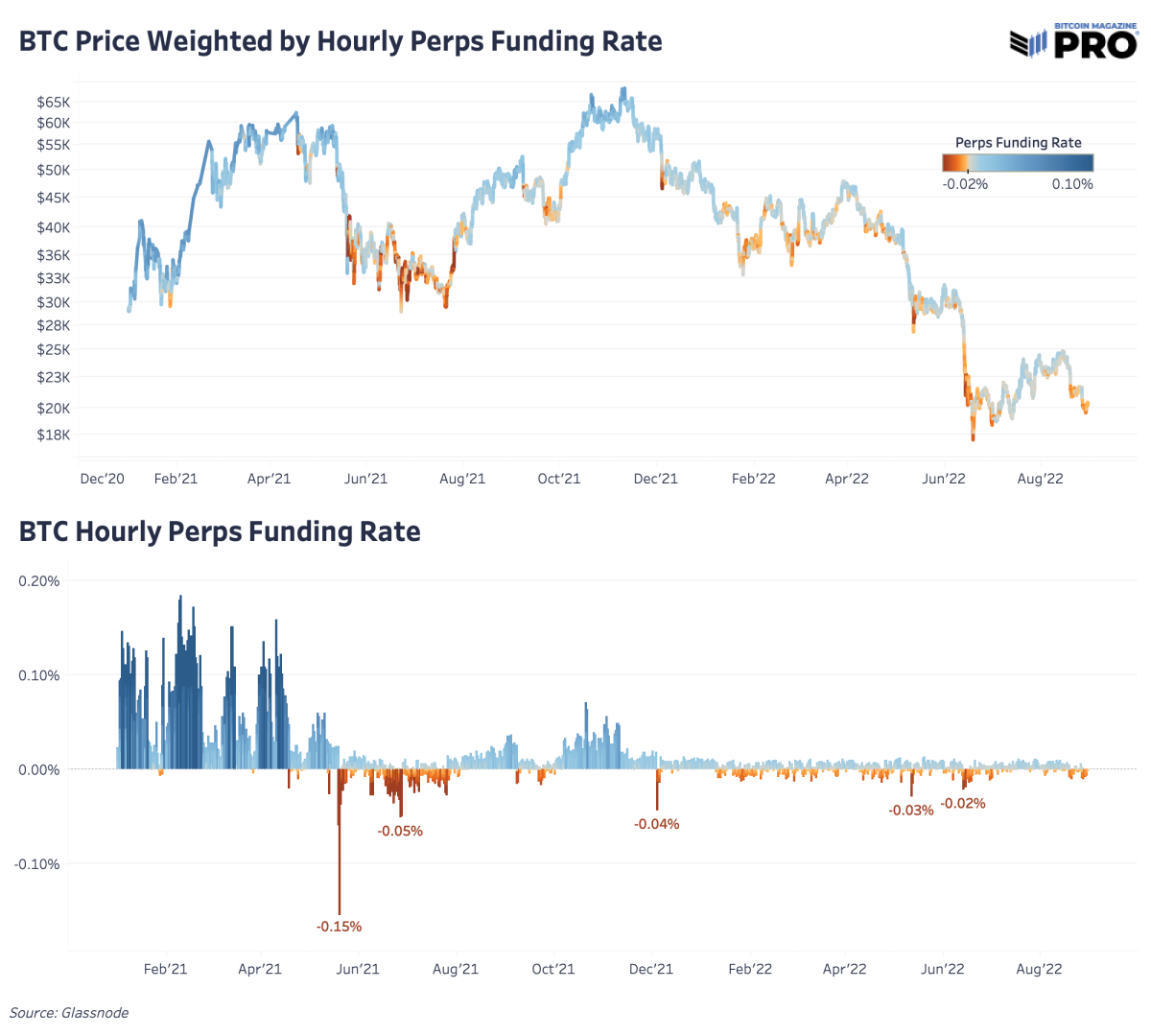

One dynamic and chart we’ve covered extensively before is bitcoin’s perpetual futures market funding rate compared to price. In the previous 2021 bull run, the perpetual (perps) futures market played a key role in moving short-term prices to both the upside and downside with excessive leverage. It’s worth reviewing the state of the derivatives market and the system’s current leverage as bitcoin price has broken down from its latest rally, following U.S. equities on a potential path towards new lows.

Since the top in November 2021, the perpetual futures market has been consistently biased towards the downside (neutral funding rate is 0.10%). Simply put, more of the market participants were and still are biased short over the last eight months. Even during the latest bear market rally move, that hasn’t changed. We didn’t see the funding rate go above neutral territory showing a clear sign that long speculators and risk appetite have not returned to the market.

With the successful launch of a bitcoin futures ETF in U.S. markets last fall, along with a general unwind in speculative activity across the bitcoin/cryptocurrency market, perp funding rates have been teetering from a neutral to short bias with much less explosive moves in funding rates. Although derivatives market dynamics have changed, it’s still worth watching for an actionable signal from the perps market where the shorting bias gets heavily offside as it's shown to do throughout history marking significant bottoms. It’s worth noting that in previous bear market cycles (where new incoming spot demand was diminished by willing sellers) funding could stay negative for long periods of times, due to lack of demand to speculate/leverage the asset from the bulls.

In previous bitcoin bear markets, funding could stay negative for long periods of times due to lack of demand to speculate/leverage BTC.

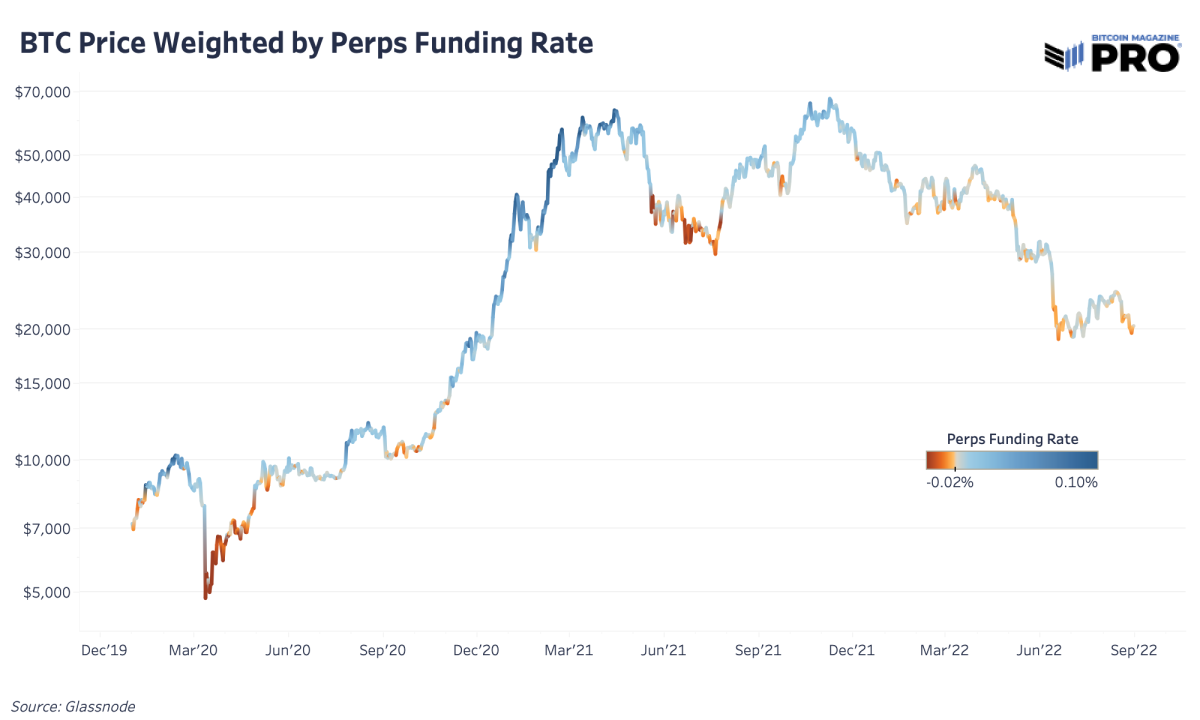

The bitcoin price weighted by the perpetual funding rate is now around its December 2020 levels.

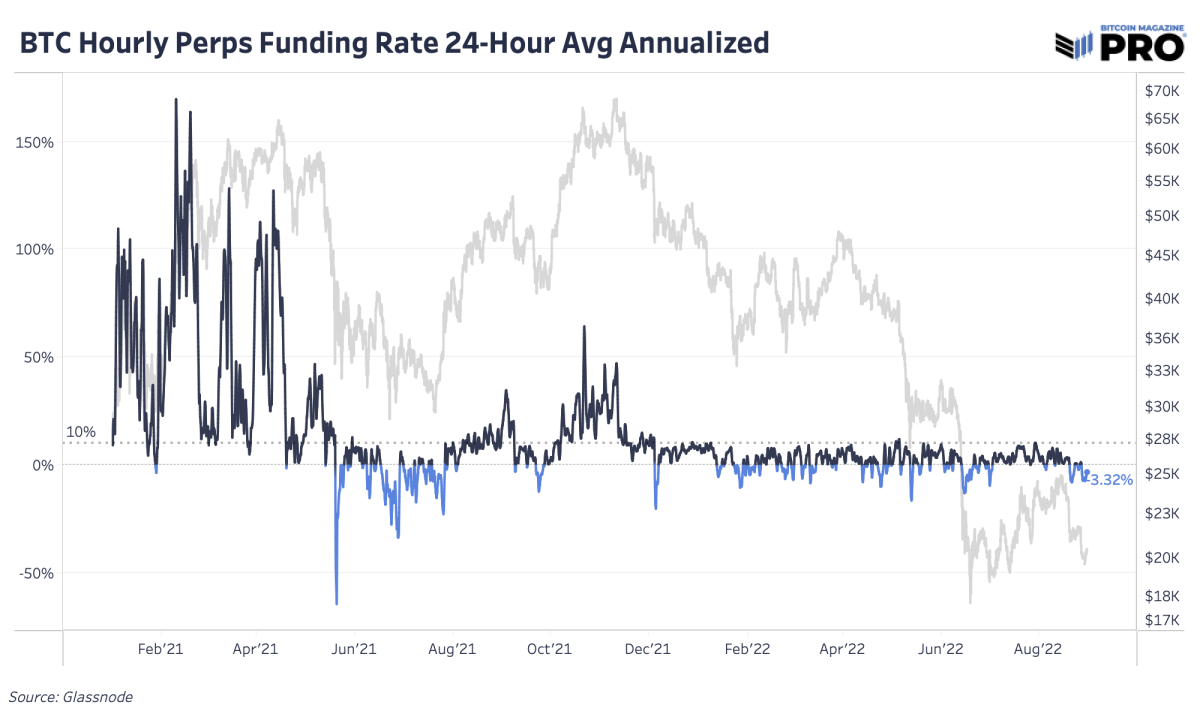

Another way to visualize the funding rate is to look at an annualized value with the current negative funding rates yielding an estimated 3.32% for taking a long against the majority of shorts. Since the breakdown in November 2021, the market has yet to get back over the annualized neutral funding rate.

An annualized value with the current negative funding rates yields an estimated 3.32%.

Price has moved with the trend of declining futures market open interest in USD since the market top. That’s easier to see in the second and third charts below which just shows the perps futures market share of all futures open interest. The perps market accounts for the lion’s share of open interest of over 75% and has grown substantially from approximately 65% at the start of 2021.

With the amount of leverage available in the perps market, it makes sense why perps market activity has such a large impact on price. Using a rough calculation of the total perps market volume from Glassnode of $26.5 billion per day (7-day moving average) versus Messari’s real spot volume (7-day moving average adjusting for inflated exchange volumes) of $5.7 billion, the perps market trades nearly five times the volume to spot markets. On top of that, daily spot volume is down nearly 40% from last year, a statistic to help understand just how much liquidity has left the market.

Given the volume of the bitcoin derivative contracts relative to spot markets, one may arrive at the conclusion that derivatives can be used to suppress bitcoin. We actually disagree, given the dynamically priced interest rate associated with bitcoin futures products, we believe that on a long enough time frame the effect of derivatives is net neutral on price. While bitcoin likely exploded much higher than it otherwise would have due to the reflexive effects of leverage, those positions eventually were forced to close, thus an equal negative reaction was absorbed by the market.