Bitcoin embodies Schumpeterian creative destruction. Bitcoin also behaves like a physical natural resource, with unique differences that make it a driving force for effecting fundamental change, much like gold, oil or electricity has done.

Bitcoin goes through periodic cycles of varying lengths that inspire a creative rejuvenation of its ecosystem with new ideas and innovations at various timescales and magnitudes. Here we will apply the idea of a Schumpeterian business cycle to Bitcoin and construct a Schumpeterian Bitcoin cycle based on three componential waves: a multi-decade Bitcoin Kondratieff cycle; a Bitcoin Juglar cycle that is shorter than a decade; and a Bitcoin Kitchin cycle that corresponds with the halvings.

Associated with these sub-cycles are three ratios that capture their logic: stock-to-flow (S2F), installed capacity-to-capital investment (IC2CI) and inventories-to-sale (I2S).

Joseph Schumpeter

1. Creative Destruction

Joseph Schumpeter would have loved Bitcoin. He would have seen in Bitcoin a living representation of his theory of capitalism, so often quoted but rarely understood. Creative destruction is the process by which capitalism continually rejuvenates itself. It is what drives markets forward and allows them to be constantly refreshed with new ideas that destroy extant structures and erect better ones in their stead.

There are countless elements in Bitcoin that structurally instill the process of Schumpeterian creative destruction in its ecosystem, making it an excellent model for the cycles of capitalistic rejuvenation that formed the basis for Schumpeter’s theory of economic growth. For instance, consider the process of the halving of block rewards. Every 210,000 blocks, Bitcoin forces a creative destruction of itself, urging its participants to either reimagine their competitive edge, seek hidden efficiencies and eradicate waste or risk being left by the wayside. Bitcoin’s worth is rooted in the intrinsic value of capitalism, liberated one cycle of creative destruction at a time.

If there is creative destruction inherent in Bitcoin, then where are all those new products that eventuate when extant markets are destroyed by new ideas? Wasn’t that Schumpeter’s point after all?

The answer is simple. Bitcoin evolves into a new product — a new version of itself — with each cycle of creative destruction. Since we are so used to thinking of a bitcoin as immutable, we tend to look past this essential characteristic feature it possesses to reinvent itself.

Bitcoin started off as electronic cash native to the Internet, but has since become many things besides. It has become the most sound platform for the definitive settlement of contracts; it has become a savings account for individuals and corporations; it has become a useful tool for international remittances; it has inspired an ecosystem of financial instruments, cryptocurrencies and much else. None of these were imagined as core features for Bitcoin in 2008. Yet, with each cycle of creative destruction, Bitcoin was reimagined.

2. A Natural Resource With A Difference

Bitcoin can usefully be examined as just another exhaustible natural resource that has held the power to alter the course of human civilization, such as gold or, even more aptly, crude oil. Crude oil underwent several cycles of creative destruction since its discovery in antiquity. In its long history, crude oil has at various times been used predominantly for heating and cooking, asphalt paving, lighting, lubricating and powering machines, transportation, plastics, aviation and so on.

Of course, there are key differences between Bitcoin and natural resources, but the similarities are just as interesting.

Bitcoin can be imagined as a physical field of exploration where prospectors dig for coins. The field has the following characteristics.

First, the total yield from the field is fixed at 21 million coins, and no matter how hard the prospectors may dig, the field simply won’t yield any more coins. All prospectors know this to be true in advance, which puts a very definite terminal point in time to their activities.

Second, prospectors know with certainty that it will get increasingly harder to find more coins as they dig. That’s because they also know that this field cannot be gated and thus prospecting cannot be regulated. So prospecting for coins will take the form of a “gold rush”; extraction of the in situ, unmined coins will be an extremely competitive activity.

Well, it will almost certainly keep getting harder. The only way in which it will ever get easier for any given prospector is if, for some reason, his rivals decide to reduce their efforts. If that happens, then for a short time the prospector gets just a bit more of the field to himself to mine for coins using his current digging equipment. Before long, though, his rivals observe his obvious fortune and come rushing back in. This squeezes him back to a smaller area on the field. Now he simply must invest in better equipment if he wishes to outcompete his rivals.

Third, the fiercer the competition, the less space each prospector will have in the field. To extract coins he will need to try even harder than before. It gets exponentially harder for him to dig deeper, and he has to bring in more and more sophisticated digging equipment to extract coins. He started off with a spoon, upgraded to a spade, then an excavator, then a vertical drill and so forth.

We paint this picture merely to underscore the point that Bitcoin is a rare and non-perishable natural resource like platinum, gold, iridium or even rhodium. It is a singular kind of natural resource even among that illustrious group, but it is one all the same. And yet, two things about Bitcoin make it a rather exceptional natural resource.

First, since available market supply is known to be fixed and the extraction rate asymptotically approaches zero, future demand is met increasingly with already obtained inventories and decreasingly through new production; until roughly 2140, after which all demand must be sufficed by a globally fixed inventory alone.

Thus, hoarding Bitcoin in inventories is rational even before all its possible uses have been discovered. Imagine if the costs of storing in inventory were similar for gold and oil to what they are for bitcoin. Now consider how we would have behaved if it were known with 100% certainty that, in the year 1850 BC, gold, or for that matter, in the year 1850 AD, crude oil had universally fixed and fully extractible supplies and that almost 90% would be extracted from all their in situ locations within just 15 years of their discovery. Hoarding would have been so frenetic and all-consuming that history books the world over would have to be rewritten.

Second, being digital, bitcoin is divisible and additive at virtually any scale and at a fraction of the cost of any physical natural resource. This makes bitcoin more “malleable” than any other natural resource, which permits its use to span markets — from micro to macro. The immutable finality of its settlement layer permits Bitcoin to function as essential macro infrastructure; the concomitant mutability that its higher layers enable permits it to function in specialized markets where contractual elasticity is required.

With this premise of bitcoin as a non-perishable natural resource, we now wish to argue that bitcoin’s market price is governed by a set of nested cycles that have been well-known to natural resource economists since at least the 1920s and were used by Schumpeter in his theory of business cycles. Their use fell out of favor in mainstream economics because of reasons that do not apply particularly well to bitcoin and, consequently, there is much that we can learn by using this framework to examine the bitcoin cycle.

3. The Three Sub-Cycles

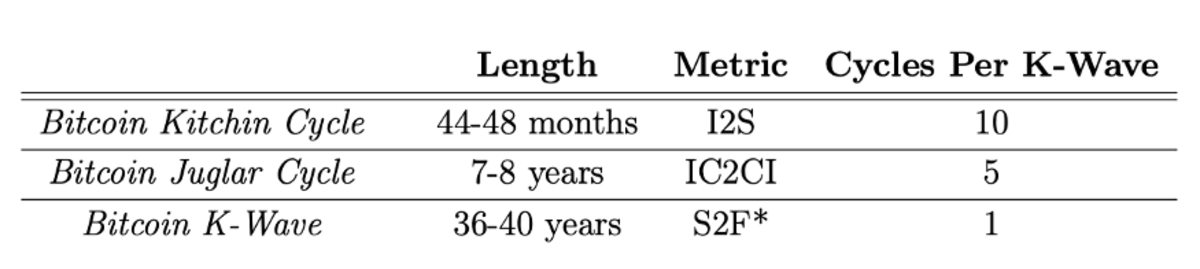

Schumpeter identified three cycles of different lengths as the basis for his theory of business cycles. Each cycle had distinct drivers and horizons, but they tended to have confluent peaks and troughs as they formed an overarching narrative for capitalistic growth; together the three cycles became the components of an overarching Schumpeterian Cycle. The sub-cycle with the shortest length in his overall three-part cycle was the Kitchin cycle, which he estimated at about 40 months, though empirically it has been measured to be as long as 60 months. The Juglar cycle was much longer, with a period of roughly 10 years (and between 7–11 years in the literature). The longest was the Kondratieff cycle (or K-wave) with a length of approximately 50 years.

What broadly drives a Schumpeterian cycle together is entrepreneurial activity and innovations interacting with one another in a grand cycle. As a suite of innovations are exploited by entrepreneurs an economy improves from a state of depression toward a state of improvement. Once the extant technology’s benefits have been leveraged at the peak of prosperity, the state of the economy turns towards recession and finally back into a state of depression.

Let’s take a closer look at each of these cycles, and explore their connection to Bitcoin.

A. The Bitcoin Kitchin Cycle

The Kitchin cycle stems from firms with fixed capital constraints that must contend with lags in information on market conditions. During the upward swing in the business cycle, firms ramp up production and enjoy super-normal profits as the market swings into prosperity. Firms bring their fixed capital use to full-employment levels and eventually overwhelm the market with excess supply. This depresses prices, tipping the market over into a state of recession. Firms respond by building up their inventories. Production gets scaled back and, once the market is back into equilibrium, the cycle is complete.

The process that drives a Kitchin cycle has been noticed in the context of agricultural commodities (in fact, it is often called the hog cycle), and led to the development of the Cobweb model to explain oscillating prices. One of us has discussed this model in the context of Bitcoin before. It is also observed in markets for hard commodities, including metals.

You might note the Achilles’ heel in the argument, if you are even casually abreast of neoclassical economics. Besides the obvious criticism of undue determinism in the length of the cycle, it minimizes the role of adaptive expectations. Firms ought to learn from the markets more effectively and not get suckered into an endless cycle of chasing demand with overproduction. Determinism is, however, built directly into Bitcoin. An average time target for blocks at 10 minutes/block over 2016 blocks is a predetermined environment variable for Bitcoin and, while miners have thus far outstripped this rate marginally, the date for the next halving can be approximated. While network difficulty and hashrates vary over the course of the cycle, and the latter is affected by market conditions on costs of production and prices, duration of the halving cycle length is known.

A Bitcoin Kitchin Cycle roughly equal to the halving cycle (44-48 months) makes sense. The supply side — miners and, to a degree, even exchanges and hodlers — is incentivized to supply more to the market as prices rise by increasing their hashrates and/or drawing down their inventories. When prices fall, miners scale back their hashrates and add to their inventories if they can or, if they cannot cover their fixed costs, they scale back or even exit.

Thus, the ratio of inventory to sales is crucial to a Bitcoin Kitchin Cycle. An inventory is a stock of a given product that the producer has access to and sales are the flows out of inventories. As selling pressure diminishes and inventories are increased, an increase in the I2S ratio marks the end of the recession phase and the beginning of the improvement phase for the following Bitcoin Kitchin cycle. The ratio falls as the cycle turns from the height of the phase of prosperity and towards the depression phase.

B. The Bitcoin Juglar Cycle

The role of innovation and investment is far more crucial in the longer duration of the Juglar cycle, where demand overwhelms the available supply during the upward phases of the business cycle so thoroughly that merely the full employment of existing physical capital is insufficient.

The pace of research and innovation increases to effect a change in the nature of new investments made by firms. Entrepreneurial effort in identifying key innovations and deploying them for such new investments takes a longer time than is permitted by the Kitchin cycle; similarly, during the downward phases of the business cycle, declining demand affects production with a greater lag than in the Kitchin cycle because new investments, once made, cannot be undone within a shorter time frame.

A period somewhat shorter than two halvings, roughly 7–8 years, seems the most natural length for a Bitcoin Juglar cycle. The first Bitcoin Juglar cycle began in 2009 and completed at the end of 2015, taking Bitcoin mining through an entire innovation and reinvestment phase from CPUs to the first broadly available ASICs. Thus, we are now approaching the end of the second Juglar cycle, perhaps sometime in 2024, and the story of this cycle, we can only hypothesize, will likely be a locational reinvestment of plants in search of energy cost efficiencies from a range of sustainable energy alternatives.

Bitcoin-friendly energy companies are already building bitcoin mining facilities next to underutilized wind energy fields producing more energy than can otherwise be consumed, as well as stranded natural gas wells that would otherwise be flared or vented. In the former case, the offtake of excess energy allows otherwise unviable wind installations to remain competitive. In the latter, greenhouse gas production from flaring and venting is reduced by bitcoin mining.

The critical ratio of interest for a Bitcoin Juglar cycle is that of installed capacity/capital investment, since it is at the peak of the cycle that the IC2CI ratio is at its highest and begins declining only as installed capacity of a specific type is overwhelmed by demand and makes the need for newer forms of capital investment more clear. Hence, the impetus for the next Bitcoin Juglar cycle comes from new capacity coming online through investments in newer technologies, production methods and materials.

C. The Bitcoin Kondratieff Cycle

The Kondratieff cycle, or K-wave, is the cycle of the longest duration, at between 40 and 60 years.

The cycle emanates from a fundamental and transformative change in technology that brings about broad socioeconomic consequences, far beyond those captured by cycles of shorter lengths. The more recent K-waves identified in the literature include the age of steel and heavy engineering (1875), the age of oil, electricity, the automobile and mass production (1908) and the age of information and telecommunications (1971).

Schumpeter, much in accordance with Kondratieff’s own vision, saw the impetus for progression between K-waves to be the clustering of several key supporting innovations. The innovative entrepreneurial insight for a transformation to begin the stage of prosperity simply could not arise unless all of the requisite ideas had first been discovered.

In the context of Bitcoin, the K-waves of concern pertain to the source of “hardness” in money. Loosely, the waves appear to be the age of gold specie money (1873–1914), the age of the gold standard (1925–1973), the age of fiat money (1973–2009) and, finally, the of age of Bitcoin (2009 onwards). If the K-wave length of roughly 40 years is prescriptive, it suggests to us that there are likely going to be interesting transformations in store for Bitcoin well before the final bitcoin is mined.

At the end of the first Bitcoin K-wave, roughly in the year 2047, 10 halving cycles would have been completed and 99.90234386% of all bitcoins would have been mined, leaving just shy of 20,508 bitcoins left to be mined. The economic value of block space will naturally rise exponentially throughout this wave and, perhaps, this metric will even prove pivotal in effecting the end of the first wave. The second Bitcoin K-wave will rely on a suite of associated technologies that are either extremely nascent at this stage or even yet unimagined in order to bring about the next transformation.

Marc Andreessen’s observation, made around the time of the beginning of the first Bitcoin K-Wave, that “software is eating the world”, is relevant to Bitcoin during this cycle since “Bitcoin is eating monetary systems”. In the second Bitcoin K-Wave, however, a much larger gamut of technologies will permit us to say that “Bitcoin is eating digital economies” en masse.

The most useful ratio for the Bitcoin Kondratieff cycle would seem to be the stock-to-flow ratio that Saifedean Ammous discussed in his book and is now well-known to Bitcoin observers thanks to PlanB’s empirical work. However, in terms of annual production and net stock, of course, the S2F ratio increases as a step-function asymptotically as we approach the year 2140. There can be no variations to accommodate cyclicality.

We concede that it may well be that bitcoin will break all expectations, as it so frequently does, and give us an age of Bitcoin that has a far longer K-wave length.

However, if indeed past proves precedent and between now and when the final coin is fully mined Bitcoin experiences at least three full Kondratieff cycles of roughly 40 years in length each, we can still use a modified version of the S2F ratio to examine the phases of each cycle; to avoid confusion, we might call it S2F*.

Within each cycle, the S2F* ratio can fall below the algorithmic equilibrium expectation if we define the “flow” as bitcoin’s market velocity in addition to its production rate per unit of time alone. A possible measure for this velocity could simply be Bitcoin Days Destroyed (BDD).

Thus, the ratio for the Bitcoin K-wave becomes:

S2F* = (extracted bitcoins held in inventory)/(annual production + BDD)

S2F* becomes identical to S2F when the majority of bitcoin inventories are dormant, which is our expectation as we move from one Bitcoin K-wave to the next. In the longer run, settlements on the base layer ought to become rarer events and indicate exceptionally significant outcomes. After all, once the land grab is behind you and the citadels have been built upon it, the emphasis shifts to the bustling activity within those structures.

In Figure 1, we summarize this section and present the three sub-cycles of the overall Schumpeterian Bitcoin cycle, their associated metrics and their approximate lengths.

Figure 1: Elements of the Three-Part Schumpeterian Bitcoin Cycle

4. And, Finally, A Look Ahead

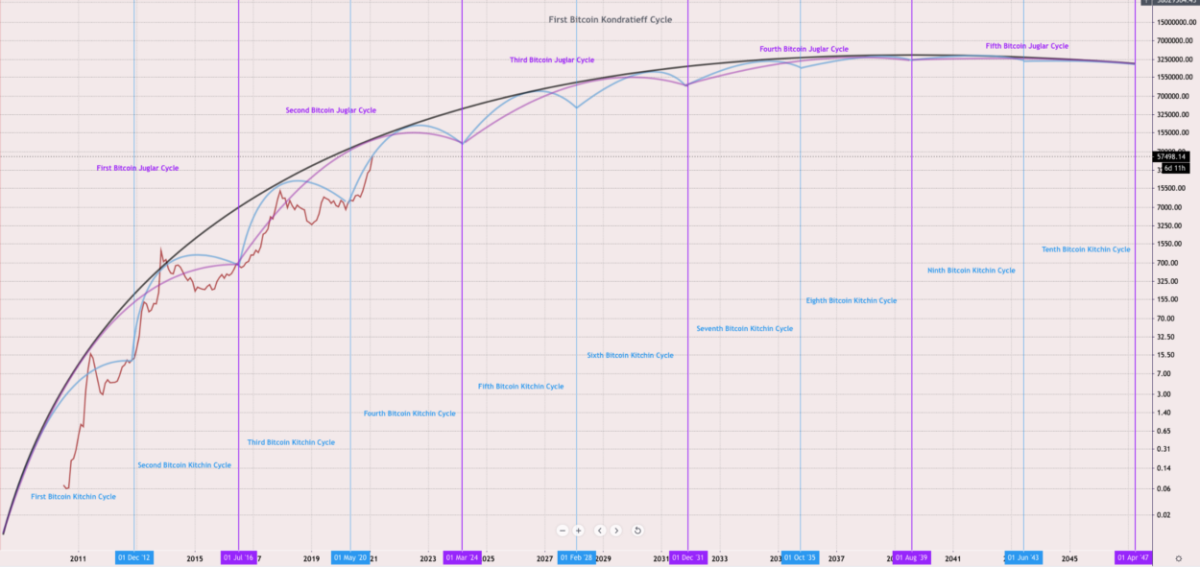

Figure 2 below illustrates the Schumpeterian Bitcoin cycle. The Bitcoin K-wave is shown in dark gray; the Bitcoin Juglar cycles are depicted in purple; and the Bitcoin Kitchin cycles, which correspond closely with the halving cycles, appear in blue.

Figure 2: Schumpeterian Bitcoin Cycle

Naturally, a dollar price as the unit of measure for the y-axis can only be taken as a very loose proxy for the various drivers of the components of the Schumpeterian Bitcoin cycle, especially considering the length of time a Bitcoin K-wave covers. However, it is worth examining a few aspects.

Towards the end of the first Bitcoin K-wave, all the cycles should converge. The idea is simply that all manner of flows out of all kinds of stocks begin to dwindle as the fundamental drivers of innovation for the next Bitcoin K-wave begin to coalesce: anew suite of technologies have arrived for Bitcoin that will become the impetus for the second Bitcoin K-wave.

Bitcoin is retained in inventories alone, and sales become rare, bringing I2S to all time highs. Capital investments dry up since the installed capacity represents increasingly untenable market propositions, driving the IC2CI ratio to all time highs. Flows of bitcoin, through mining (for obvious reasons) and from inventories peter out to extremely low levels, resulting in a stratospheric S2F* ratio. All ratios will remain relevant in the second Bitcoin K-wave, albeit at an entirely different order of magnitude.

What lies ahead is anyone’s guess…

Just like the Kondratieff waves since the industrial revolution, we should expect truly transformational innovations affecting economies and societies globally in each of the Bitcoin Kondratieff waves. Perhaps, bitcoin as the undisputed global reserve currency at the close of the first K-wave; then Bitcoin as the basis for a global digital infrastructure in the second K-wave; and, it’s hardly beyond the realm of possibility that bitcoin emerges as the basis for interplanetary transactions in the third!

This is a guest post by Prateek Goorha and Andrew Enstrom. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc. or Bitcoin Magazine.