For decades, the velocity of money, which is a measure of the times that a unit of currency is spent, has fallen due to what some economists have termed the “safe asset shortage.” This has occurred for a variety of reasons, including aging demographics in advanced economies and lack of trust in governmental institutions in emerging economies.

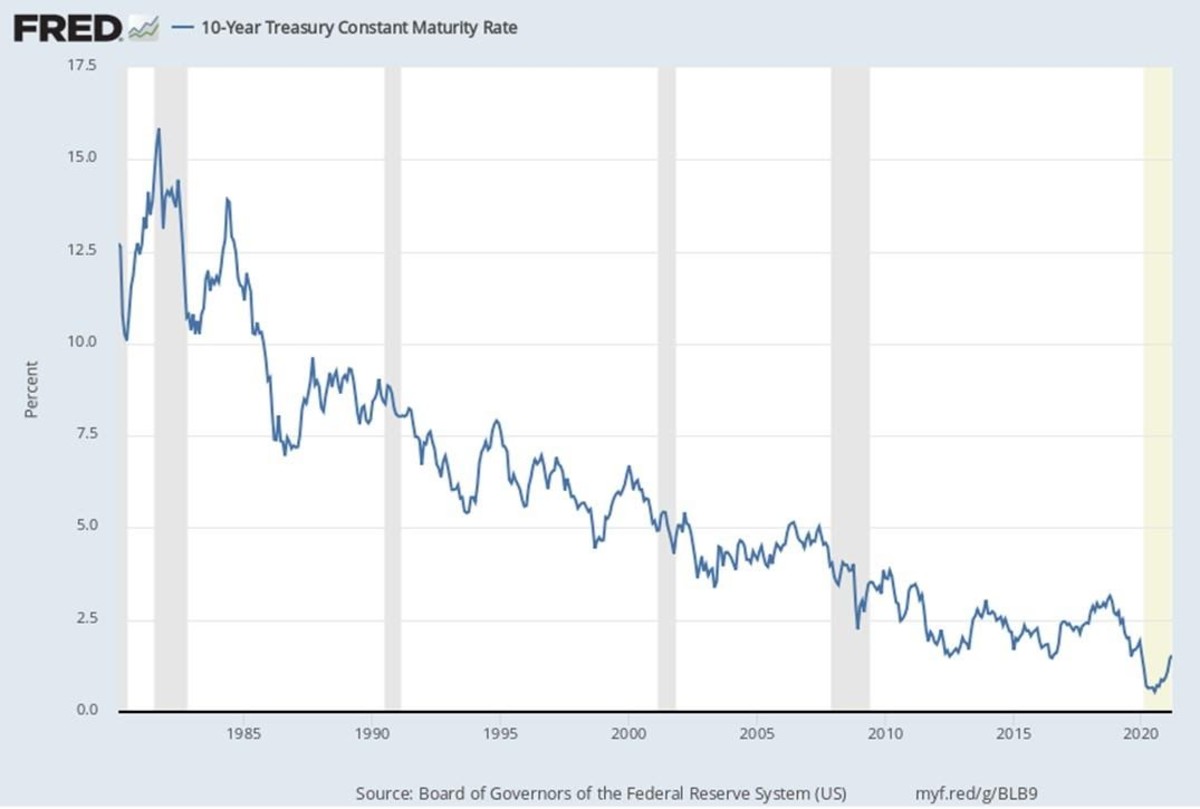

The safe asset shortage could be described, in simple terms, by saying that the demand for safe assets (cash and government bonds) is not keeping pace with the growth of overall wealth. As a result, demand for these assets has driven down global interest rates for decades (see chart below) creating a liquidity trap — a condition where yields on government bonds and cash are so close that many prefer to hoard cash. This means that, as money is created by central banks, much of it essentially becomes locked away on private balance sheets (bank, corporate and individual) to satisfy the demand for liquid savings. Failure of governmental institutions to produce enough safe assets has contributed to the falling monetary velocity, slow growth in the Eurozone and Japan and structural lack of labor in the United States.

But what if this demand for savings could be satisfied by something other than government bonds or currency? Enter Bitcoin.

As cited by David Andofatto of the St. Louis Federal Reserve in his blog post entitled “Is Bitcoin A Safe Asset?,” bitcoin “…could be the world’s next great safe asset. At least, it certainly seems to have all the properties that are desired in a safe asset.”

The blog goes on to describe some of Bitcoin’s attributes, including its simple monetary policy and fixed supply, with the implication being that this is a role that bitcoin could serve.

But to be clear, it is not there now, so this is a stretch goal for bitcoin. But if we zoom 20 years into the future and assume tht the bitcoin market capitalization reaches maturity ($20 trillion-plus), its volatility will likely stabilize as sales and purchases totaling many billions of dollars each day would fail to spike or crater the price.

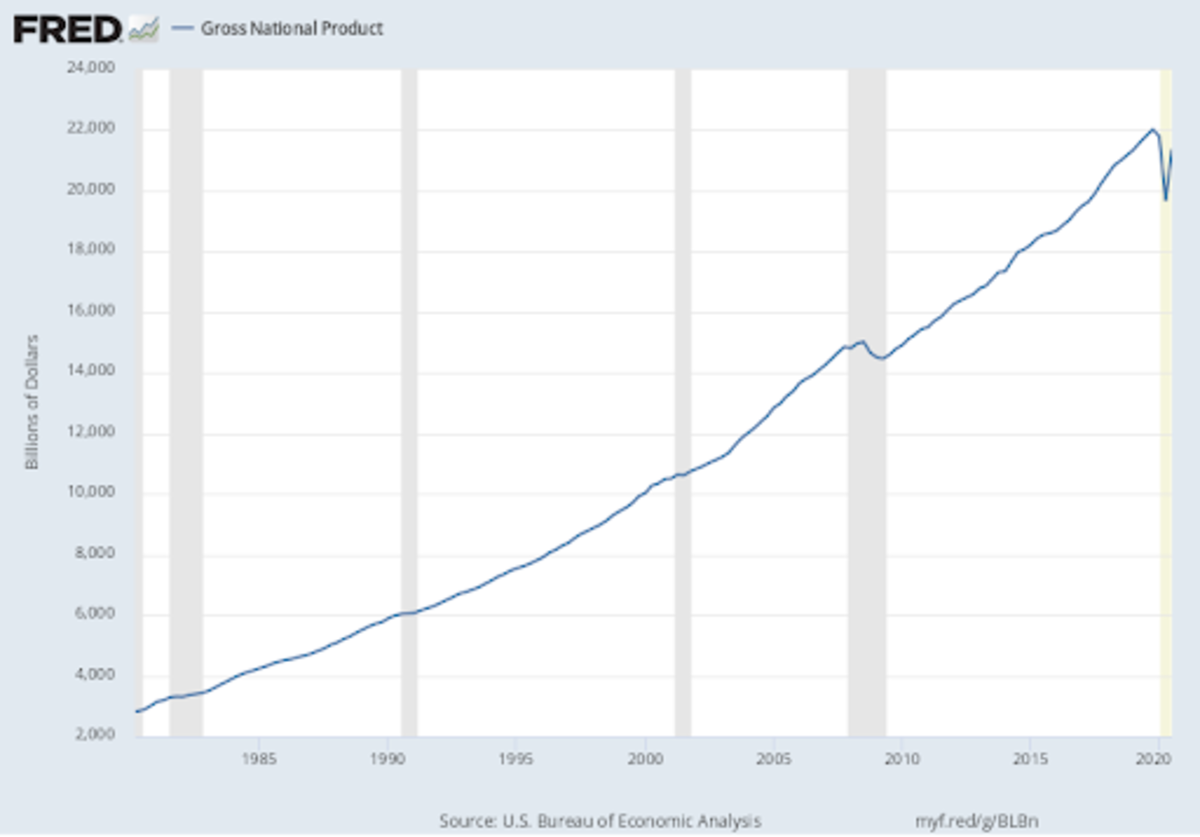

Under such circumstances, as a safe asset, bitcoin could be expected to appreciate near the rate of nominal GDP, say 4 percent to 6 percent per year, on average (see chart below). That is, as the number and price of goods and services expands globally, after several more bitcoin mining subsidy halving cycles, the total supply of new bitcoin barely increases — increasing numerator, fairly constant denominator. Boring for traders, but ideal as a safe asset.

So, how would bitcoin solve this problem? Essentially, I am arguing for a type of currency duopoly. Bitcoin could effectively soak up much of the demand for long-term savings, and fiat would still be used for everyday spending.

The key here is that the global economy would no longer rely as much on the production of safe assets by governments. Because bitcoin is not debt-based like government bonds or bank deposits, it is not constrained by interest rates falling to the zero lower bound. Any increase in demand for bitcoin is accommodated by a corresponding increase in price. This does not mean bank deposits won’t still exist or that governments won’t issue debt. Both will persist, but their rates and term structures would need to reflect the availability of another highly-liquid, non-governmental, safe asset: bitcoin.

Those who argue that bitcoin will someday be used ubiquitously for spending are ignoring that bitcoin’s properties make it ideal for hoarding. Why spend bitcoin when you could spend fiat instead? Some would claim this dual currency theory is far-fetched, yet I would argue currency duopolies exist all over the globe today.

Go to any third-world country and you will find people there who are eager to receive U.S. dollars for payments, which they save, while they spend their local fiat. They lack faith in their governmental institutions to preserve the value of their local currencies. It is not unreasonable to therefore assume that bitcoin could serve this role globally across all economies, including the U.S.

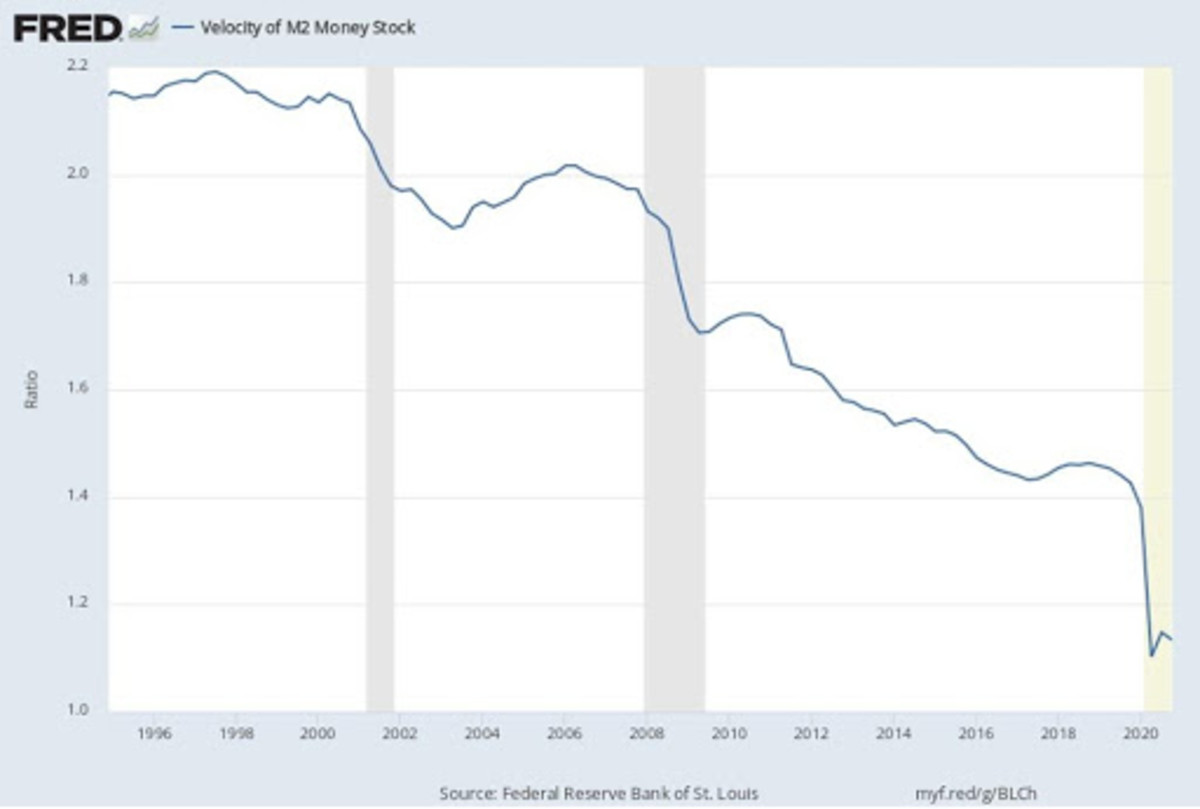

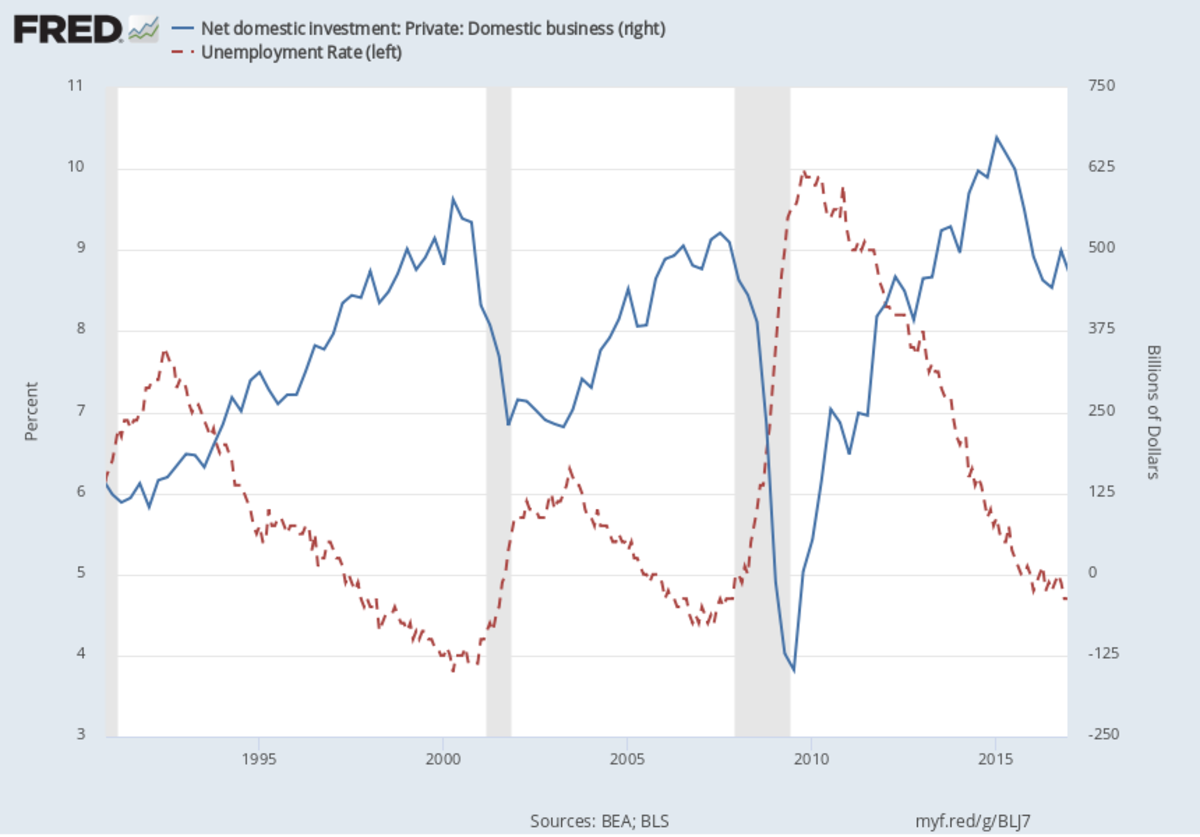

As bitcoin replaces fiat and debt as a vehicle for saving, central banks globally would need to produce less fiat to satisfy the demand for liquid savings, and the problem of monetary velocity falling for decades could potentially be solved (see the M2 velocity chart below). As monetary velocity accelerates again, incomes go up because one person’s spending is another’s income. And when incomes go up and labor markets get tight, businesses have incentive to invest in new products and services, as well as to enhance the productivity of existing workers. Business investment is pro-cyclical. That is, it peaks when the economy is running near its potential, and as unemployment falls, investment rises (see the net private domestic investment chart below). In short, when the virtuous cycle of money flows is reestablished, prosperity could be felt more widely.

To be clear, this rosy picture is a long way from reality, but we are seeing seeds being planted today, as a small number of corporations and individuals have chosen to replace their fiat savings with bitcoin. It is not illogical to think this trend will continue.

The implication for central banks is that, when fiat is created, it will be more quickly spent, resulting in more effective monetary policy. For governments, a currency duopoly creates no threat to government power. It can still borrow and spend fiat into the economy as needed to achieve its goals (provide for the common defense, infrastructure, social safety nets, etc.). Indeed, the presence of U.S. dollars or debt does not prevent Mexico, or any other foreign government, from carrying out its day-to-day duties. In my view, the emergence of bitcoin would be a clear winner for all involved.

So, why is no one writing about this potential benevolent future? I suspect most bitcoiners do not understand monetary economics or the safe asset shortage, and most academics are loath to discuss “crazy” bitcoin in general.

Perhaps the Austrian economists will counter that bitcoin will drive out all other forms of money and the Modern Monetary Theorists will claim that only government can give currency value. Heck, even mainstream economists may disagree on the extent to which the safe asset shortage is a problem or a symptom. Those aside, my aim with this article is to facilitate the discussion. These are admittedly complicated subjects that I am simplifying — a lot. But hopefully, in due time, more economists will start taking bitcoin and its broader economic implications a bit more seriously.

This is a guest post by Monetary Wonk. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.