Introduction

A group of shareholders of the Grayscale Bitcoin Trust (GBTC) have banded together in the first-of-its-kind activist campaign organized through X (formerly Twitter). Their goal: bringing legal action against Grayscale in an attempt to force them to allow redemptions for customer cryptocurrency held within the trusts it operates and to repay “exorbitant" management fees.

Though initially a grassroots campaign, one of the largest GBTC and Grayscale Ethereum Trust (ETHE) shareholders, Alameda Research, has filed a lawsuit against Grayscale with numerous funds joining as plaintiffs: Fir Tree Partners, Saba Capital, Owl Creek Asset Management, UTXO Management and Aristides Capital. The complaint was filed in Delaware’s Chancery Court, with the assertion that Grayscale has breached its “contractual and fiduciary duties to Alameda and other trust investors.” The specific cause for complaint accuses Grayscale of charging excessive fees in addition to its refusal to allow for the redemption of bitcoin and ether. According to the court documents, Grayscale has charged over $1.3 billion in fees in the last two years alone. The plaintiffs are seeking to claw back those funds as well as renegotiate the fee structure of both GBTC and ETHE to “competitive rates.”

The participants in the Grayscale lawsuit created a website in order to gather additional shareholders to join their fight due to the trust documents which state that shareholders only have the right to bring a case like this one against the trust if unaffiliated parties collectively holding at least 10% of outstanding shares join together as co-plaintiffs.

The Grayscale Litigation website has additional details for those wishing to sign up to participate in the legal battle or for those wanting to find out more about the campaign. The initial deadline for joining the litigation is Sept. 1, with the last day by which Alameda is to respond to Grayscale’s motion to dismiss scheduled for Sept. 15.

The above is an overview of the case, but there are multiple related entities and nearly as many active lawsuits against the web of companies that operate and facilitate the trust, as well as one current case against the Securities and Exchange Commission (SEC) brought by Grayscale.

To fully understand the complexities, it’s helpful to step back and examine the structure and formation of GBTC as well as the events leading up to the lawsuits.

How Does GBTC Work?

Grayscale runs multiple cryptocurrency trusts with the most well known examples being GBTC and ETHE. These trusts operate similarly to each other, with Grayscale as the sponsor that manages the trust, including management fees and how they themselves can be replaced with a different sponsor. Shares of the respective trusts are issued by an authorized participant. In this case, the authorized participant of these trusts was for many years Genesis, an affiliate of Grayscale. Both companies are subsidiaries of the same parent company, Digital Currency Group (DCG).

In order for shares to be issued, interested parties had to deposit bitcoin (or ether) with Genesis, which then placed the assets into the trust and created shares that were locked up for a period of six months. After this six month period, the shares were considered seasoned and were able to be transferred to another party or sold in the secondary market.

These are currently one-directional trusts, meaning that the bitcoin (or ether) only goes into the trust and cannot currently be redeemed by surrendering shares. While Grayscale has claimed that they are not legally allowed to redeem shares, the legal complaint says that the firm has contradicted this by admitting that Regulation M under federal securities law does in fact provide approval for allowing redemptions so long as there is no ongoing share creation.

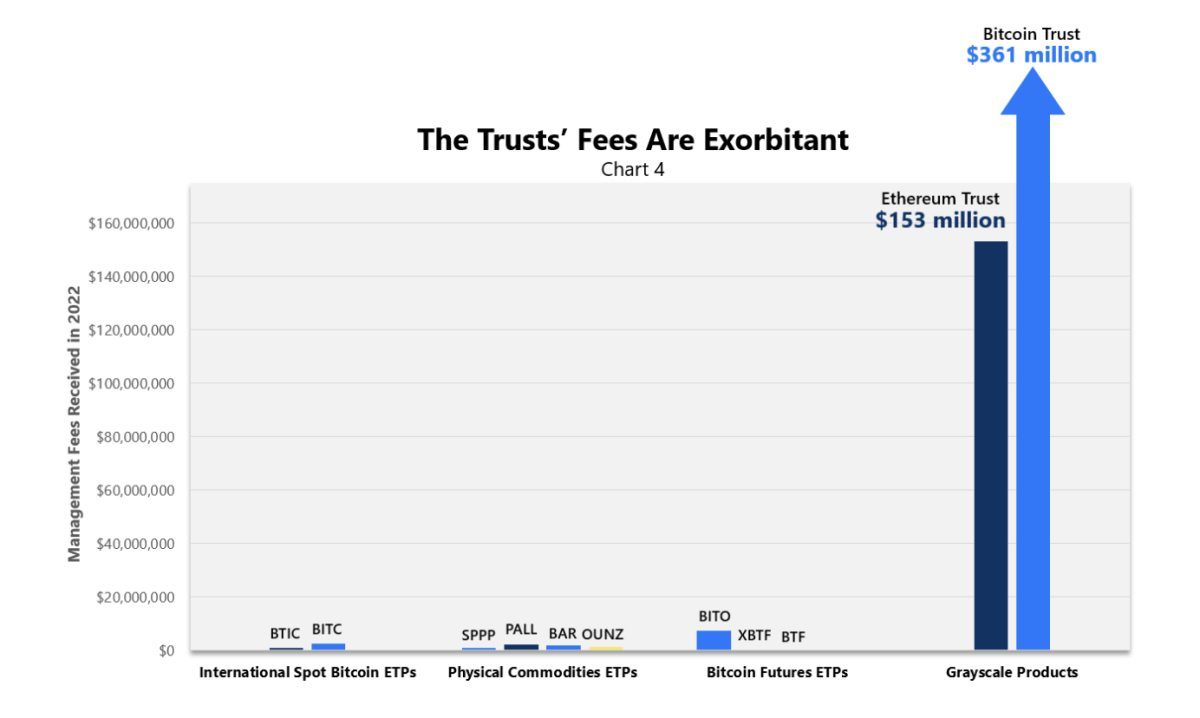

As the market grew, GBTC’s holdings peaked at roughly 650,000 bitcoin, the largest known single holdings of bitcoin in the world. The market value of that bitcoin is worth over $17 billion at the time of writing. Regardless of whether the shares are trading at a premium or at a discount, Grayscale receives 2% of the total bitcoin holdings on an annual basis as management fees. This equates to roughly 13,000 bitcoin, or nearly $350 million, in revenue from fees per year, making Grayscale extremely lucrative. These fees do not factor in the company’s other cryptocurrency trusts. Currently, there are approximately 624,366 bitcoin remaining in the trust.

In the past, the price of GBTC loosely followed the bitcoin price, but due to the six month lockup period, the share price became uncorrelated to the underlying bitcoin sitting within the trust. There were times when the trust traded at a premium of nearly 50%, meaning that the value of a share was being valued much higher than the equivalent bitcoin held in trust. This was positive for shareholders who could sell their shares at a price higher than the value of the underlying asset. However, in February 2021, shares no longer traded at a premium and instead traded at a discount below the net asset value (NAV). At their lowest point, shares were trading at nearly a 50% discount and continue to trade at a discount to this day, costing shareholders billions of dollars in lost share price value.

The peak of the GBTC premium was nearly 50%. At the lowest point, the discount to NAV was also nearly 50%.

At the current discount of GBTC shares to NAV, the implied bitcoin price is $19,546, nearly $10,000 less than the current spot value.

Why Would Someone Invest In GBTC?

Bitcoin is not often traded in traditional brokerage accounts, so investors who primarily trade through institutional exchanges, such as Charles Schwab or TD Ameritrade, would not be able to use their investment portfolio to purchase bitcoin. This includes those with 401(k) or individual retirement accounts.

Since there is not currently a spot bitcoin ETF for investors to get exposure to bitcoin, and especially during the times when GBTC was trading at a premium, buying shares in Grayscale’s trust was touted as a wise investment. If they wanted to invest directly in bitcoin, the only alternative option for investors with retirement accounts would be to liquidate their accounts and pay an early withdrawal penalty before being able to buy bitcoin on an exchange with the no longer tax-advantaged funds.

From its inception, Grayscale has always stated its intention to convert the trust into an ETF and is in active litigation against the SEC about this matter. An ETF product in the U.S. has to get approval from the SEC, whereas the company’s current trust structure does not require the same level of regulatory approval. Grayscale created this trust to allow people to buy bitcoin who otherwise wouldn’t be able to and it was considered a very innovative model at the time of its formation in 2013.

Grayscale was able to charge a relatively high annual fee of 2% for GBTC because this trust was a unique investment vehicle. Investors who were unable to gain bitcoin exposure in other ways were willing to pay this fee, especially if their shares could be traded at a premium to NAV. In recent years, these fees have become higher than competitive rates, as the lawsuit details.

Cryptocurrency Contagion

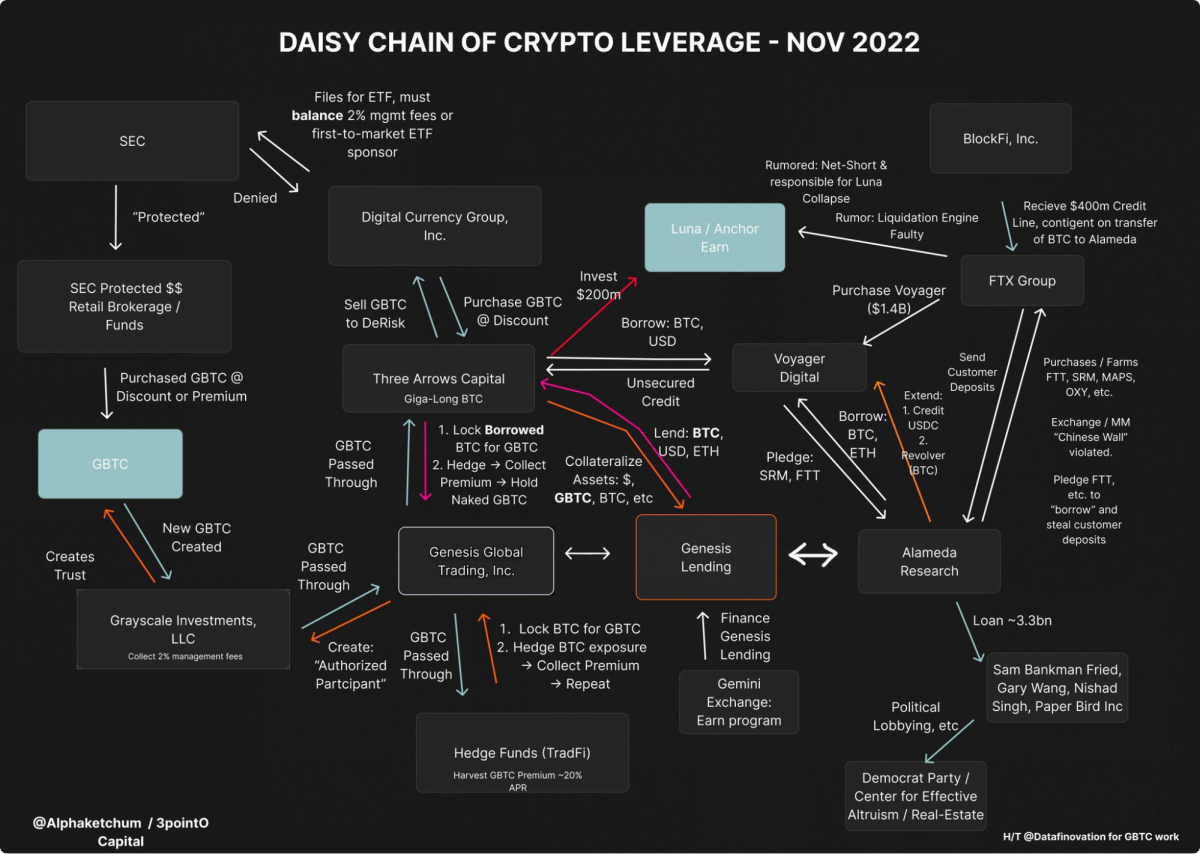

A relevant part of the story is that Grayscale’s original authorized participant, Genesis, was lending millions of dollars to hedge funds, like Three Arrows Capital, allegedly on the condition that they parked the money in the Grayscale Trusts. In June 2023, after GBTC started trading at a discount, Three Arrows Capital blew up, sparking a wave of contagion events that bankrupted multiple cryptocurrency companies, such as Babel Finance, Voyager, BlockFi and FTX.

When Genesis filed for Chapter 11 bankruptcy in January 2023, it owed creditors over $3.5 billion. The graphic below demonstrates the convoluted chain of leverage among various cryptocurrency hedge funds, which allowed them to capitalize on the GBTC premium trade, thus creating an outsized Genesis lending book and ultimately leading to the crypto contagion in 2022.

Source: Alfaketchum

The Grayscale Lawsuit

In addition to Alameda, there is a group of GBTC shareholders organizing in order to take action against Grayscale with the hopes of clawing back hundreds of millions in fees, renegotiating the fee structure moving forward and being granted the ability to redeem the customer bitcoin held in the trust. This lawsuit is a derivative action, meaning that it affects all shareholders and not just the shareholder filing the lawsuit.

To even be able to file a derivative action against the trust, multiple unaffiliated shareholders who jointly own at least 10% of shares outstanding need to join together as co-plaintiffs to bring the lawsuit, according to trust documents and Grayscale’s related arguments.

The shareholders accuse Grayscale of mismanagement and conflicts of interest. The conflicts of interest relate to all critical parties associated with the trust being subsidiaries of DCG: Grayscale as the sponsor, Genesis as the authorized participant and CoinDesk as the index provider for the bitcoin price. Other firms have offered to take over operation of the trust at a lower management fee that is more in line with industry standards, including Valkyrie Investments who published a letter offering to manage the trust with an annual fee of 0.75%.

In his end-of-year letter to investors, Grayscale Investments CEO Michael Sonnenshein stated, “We remain steadfast in our belief that the conversion of GBTC to an ETF is in the best interest of investors, and we remain 100% committed to that endeavor.” While he shared plans for a potential 20% tender offer, should that not be possible, the company “would instead continue to operate GBTC without an ongoing redemption program until we are successful in converting it to a spot bitcoin ETF.” This is in line with the company’s claims that they are unable to allow redemptions without express permission by the SEC and are only focused on their lawsuit against the SEC to allow the conversion of the trust into an ETF.

With shares trading at such a large discount and redemptions not allowed, shareholders are trapped unless they sell their shares at a considerable loss. Notable Bitcoin critic, Congressional Representative Brad Sherman, wrote a letter to SEC Chair Gary Gensler seeking clarification from the agency as to whether Grayscale is actually prevented from allowing redemptions. He also questions the company’s lack of an independent director on its board and its comparatively high fees, among other regulatory concerns.

The Alameda bankruptcy estate is leading a derivative action against Grayscale, claiming the sponsor has collected $1.3 billion in management fees in violation of its trust agreement. In a motion filed in the Delaware Chancery Court, Alameda said that it had assembled over 45 parties, including dozens of individuals, numerous funds and family offices, who indicated they were willing to participate as additional plaintiffs.

The motion details how the plaintiffs believed they reached the 10% threshold of shares, that is until a large shareholder who was expected to be a plaintiff dropped out without explanation, leaving Alameda below the necessary share count. The court granted the plaintiffs until Sept. 15 to gather the remaining support from shareholders.

The plaintiffs are putting out a call to any and all GBTC shareholders who are interested in joining the Grayscale lawsuit. Their website has more information and an intake process where shareholders can sign up before Sept. 1 to participate in the legal case against Grayscale.

Disclosure: David Bailey is the CEO of BTC Inc., the parent company of Bitcoin Magazine and UTXO Management. UTXO Management is a plaintiff in the Grayscale Litigation.