The below is from a recent edition of the Deep Dive, Bitcoin Magazine's premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

The subject of today's Daily Dive will be the playbook that is seemingly being followed by G7 governments and global central banks. While some may be skeptical that there is a coordinated campaign or playbook, the following paper released by the International Monetary Fund (IMF) in March 2011 may persuade you otherwise.

The paper, “The Liquidation of Government Debt,” outlined how governments and central banks could go about reducing public and private debts. Below is the abstract of the paper.

Abstract

“Historically, periods of high indebtedness have been associated with a rising incidence of default or restructuring of public and private debts. A subtle type of debt restructuring takes the form of “financial repression.” Financial repression includes directed lending to government by captive domestic audiences (such as pension funds), explicit or implicit caps on interest rates, regulation of cross-border capital movements, and (generally) a tighter connection between government and banks. In the heavily regulated financial markets of the Bretton Woods system, several restrictions facilitated a sharp and rapid reduction in public debt/GDP ratios from the late 1940s to the 1970s. Low nominal interest rates help reduce debt servicing costs while a high incidence of negative real interest rates liquidates or erodes the real value of government debt. Thus, financial repression is most successful in liquidating debts when accompanied by a steady dose of inflation. Inflation need not take market participants entirely by surprise and, in effect, it need not be very high (by historic standards). For the advanced economies in our sample, real interest rates were negative roughly ½ of the time during 1945-1980. For the United States and the United Kingdom our estimates of the annual liquidation of debt via negative real interest rates amounted on average from 3 to 4 percent of GDP a year. For Australia and Italy, which recorded higher inflation rates, the liquidation effect was larger (around 5 percent per annum). We describe some of the regulatory measures and policy actions that characterized the heyday of the financial repression era.”

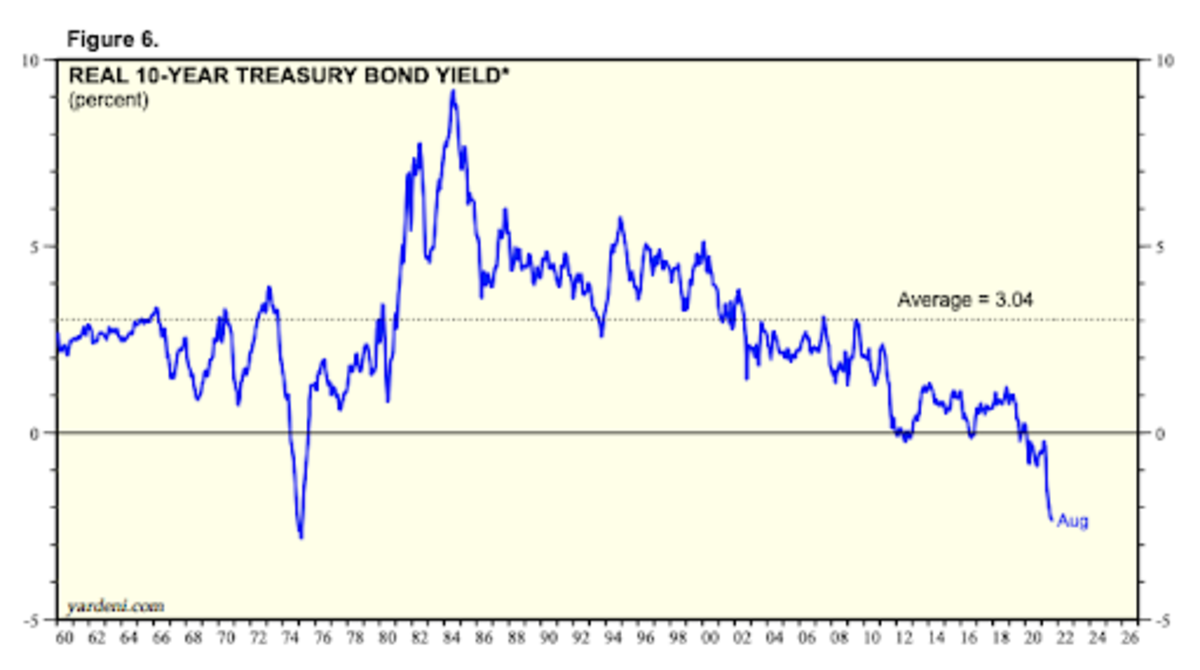

The most alarming aspect of the paper is the fact that the playbook laid out a decade ago seems to be being followed to a tee. Most specifically, financial repression by capping interest rates while letting inflation run hot.

With the consumer price index (CPI) continuing to run far above the Federal Reserve funds rate, real yields are negative across the treasury yield curve. In other words, bond holders are getting their interest payments while their principal decays in value (refer to abstract: “financial repression includes directed lending to government by captive domestic audiences [such as pension funds]”).

Source: Yardeni