Three months have passed since the People’s Bank of China (PBOC) issued an official statement explicitly defining initial coin offerings (ICOs) as illegal public financing activities. As a result, all China-based ICO projects were required to refund all initial investments, regardless of whether or not project-based tokens were issued; foreign-based projects were required to refund investors as long as the tokens had not been issued; and more importantly, all China-based bitcoin exchanges, including Huobi, OKCoin and BTCC, shut down. The reason given for shutting down: pressure from “related government departments.”

Pessimists believed this would herald the end of Bitcoin in China — and even around the world — a sentiment that has been enhanced by the astonishing plummet of bitcoin price on Chinese exchanges from around $7,400 to as low as $2,400. And, as usual, whenever rumors float out of China, markets react — whether those rumors are based entirely, partially or not at all in truth.

As bitcoin exchanges in China shut down, public trading volumes of Chinese Yuan became literally zero; therefore, any news from China related to Bitcoin should be irrelevant to the price. Bitcoin’s ferocious bounce-back to nearly $8,000 in mid-November 2017, an all-time high, confirmed the point that no matter what is going on in China and regardless of Chinese hurdles, the price of bitcoin will continue its ascent.

But there is an exception: mining.

Will Mining Be Shut Down?

China is still the largest host country for mining facilities. Indeed, 70 percent of hash power globally comes from Chinese mining pools. The miners produced by Chinese company Bitmain dominate the whole industry.

People worry about whether the Chinese government will ban mining, thereby eliminating Bitcoin from China at its source and throwing the ecosystem into disarray. However, this is highly unlikely.

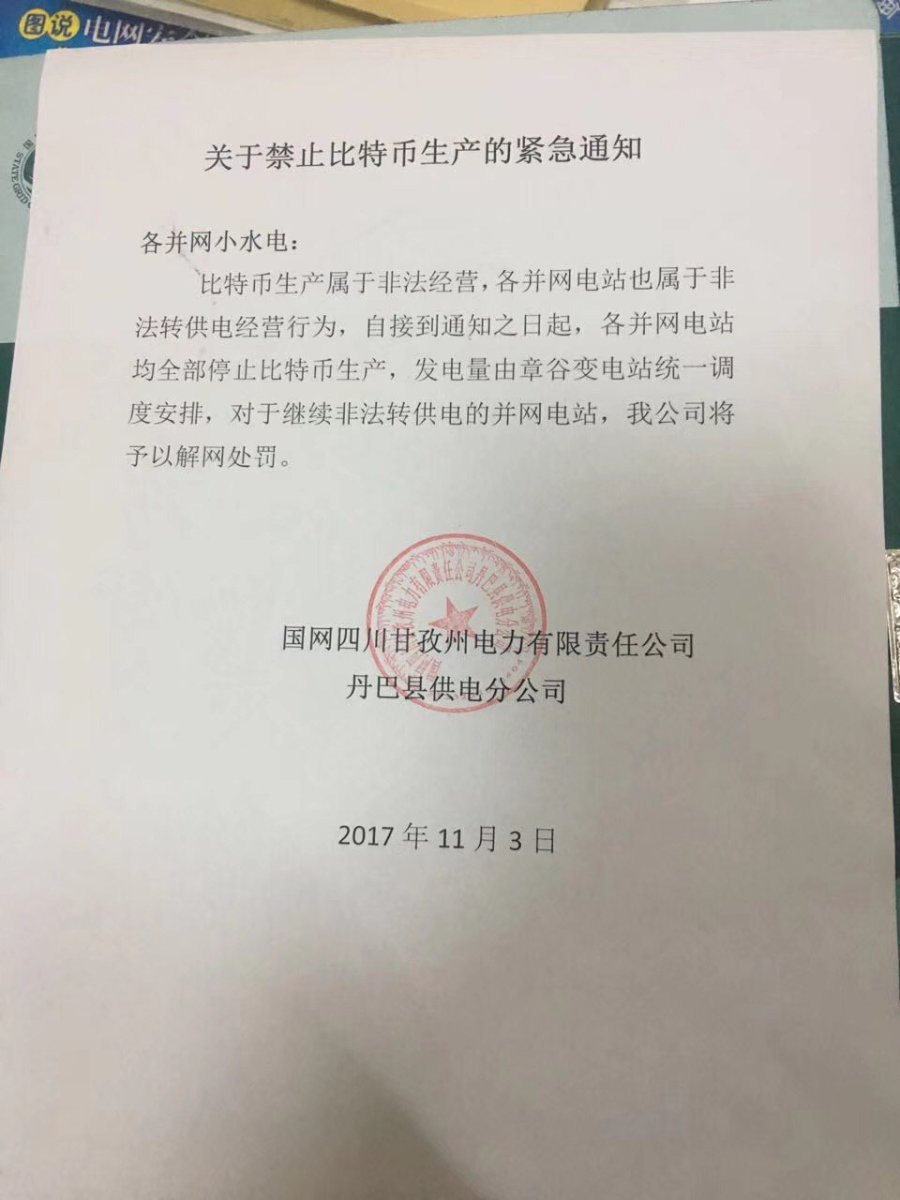

The recent rumor that a mining ban is becoming a reality was derived from a flyer, distributed by a power station in the Chinese province of Sichuan. The flyer stated, “Bitcoin is illegal thus the company shall not provide electricity to mining facilities.”

In fact, this flyer is nothing more than a poorly worded, company-level notice that mistakenly used the word “illegal.” The content, however, has since been misconstrued as proof of an official ban on Bitcoin mining.

An internal notice by a local power station stating that “bitcoin production is illegal”

The financial desk of Caixin — a reputable Chinese news source — and several citizen-based media sources have interviewed the power company in question. These sources have since confirmed that this interpretation is nothing more than overhyped “fake news.” The notice was meant for internal use only. Its chief aim was to warn its affiliates about the risks associated with providing illegal electricity. The power station and its affiliates can generate electricity but have not secured the requisite approval from the government to sell electricity to anyone — not just miners.

It is important to reiterate that China has never denounced Bitcoin as illegal. Bitcoin itself in China is regarded as a type of good. “People have the freedom to participate [in] bitcoin trading as type of goods on the internet,” a PBOC notice stated in 2013. Therefore, the government has no reason to shut down the “factories” producing normal “goods.” While it is true that there are reports circulating that mining facilities are facing the pressure of possible suspension, the reason for this pressure is related to their illegal use of electricity, not mining activities.

More convincingly, Caixinreported on October 13 that “a person close to the regulator said to Caixin that China has no plan to ban mining.”

Lastly, there is a good chance that China could decide to create its own regulated Bitcoin trading market. If these plans become a reality, China is even less likely to ban mining.

There are two reasons why this theory may be valid. First, China is highly motivated to enter the trading market. Japan has licensed several cryptocurrency exchanges, and CME is stepping up efforts to list bitcoin futures to build a more regulated trading market.

China, as the second-largest economy, has good reason to want to build its own regulated market, too. The logic is that as bitcoin trading can’t simply be banned by any single government due to its decentralized nature, banning it will only result in uncontrollable OTC trading that might result in more hidden-capital flight. This is the last thing that the Chinese government will want to see. Therefore, both external pressure and Bitcoin’s internal features will drive China to think about a better mode of regulation.

Second, Caixin also hinted that a more regulated bitcoin market in China might be possible in its article titled “Will Bitcoin Come Back to China After China Becomes Less Relevant to Bitcoin?” The article ends with: “Maybe someday when regulators find a better way to regulate Bitcoin, we can’t preclude the possibility that Bitcoin will come back to China.”

Caixin holds a special status among all media sources for the Chinese Bitcoin industry. It has long been the primary source for regulation and policy signals from the PBOC: It has literally become the mouthpiece for the PBOC in regard to regulating Bitcoin. The fact that this sentiment was allowed to be published under such tightly controlled circumstances makes it particularly interesting and relevant.

Blockchain Development Still Going Strong

The reputation of blockchain technology, which underlies Bitcoin itself, has been stained by the speculation side of bitcoin and alt coins to some extent. But luckily, the development of blockchain technology is still an important directive and priority for China.

According to China’s Premier Li Keqiang last year ― in the government’s 13th Five-Year Plan for Economic and Social Development ― blockchain technology has been listed as an important area of development for Chinese endeavors. As long as this remains the case in China, we can expect to see overall favorable conditions for accelerated growth in the industry.

Chinese blockchain startups are beginning to expand their communities overseas, and Chinese exchanges have launched international sites. Investors, though less than before and less openly, are still committing to blockchain-based enterprises. Consortium blockchain solutions are being welcomed by big companies. In short, there is more rationality and less speculation.

In fact, the so-called ICO ban is actually just an announcement, rather than a specific law. There is a very subtle balance between the industry and the regulators. The industry is testing governmental and regulatory boundaries as it reaches toward more autonomy. The government, for its part, is observing whether the industry really will live up to its revolutionary promises and is deciding on the best way to encourage innovation while also avoiding speculation risks.

The blockchain industry needs to win regulators’ trust by actually solving commercial pain points to prove that token-oriented models are feasible. If no project can prove this and tokens still remain a tool of pure speculation, the industry simply can’t expect looser policies. It is up to the crypto and blockchain community to live up to its promise and deliver the innovation that the modern world needs and expects.