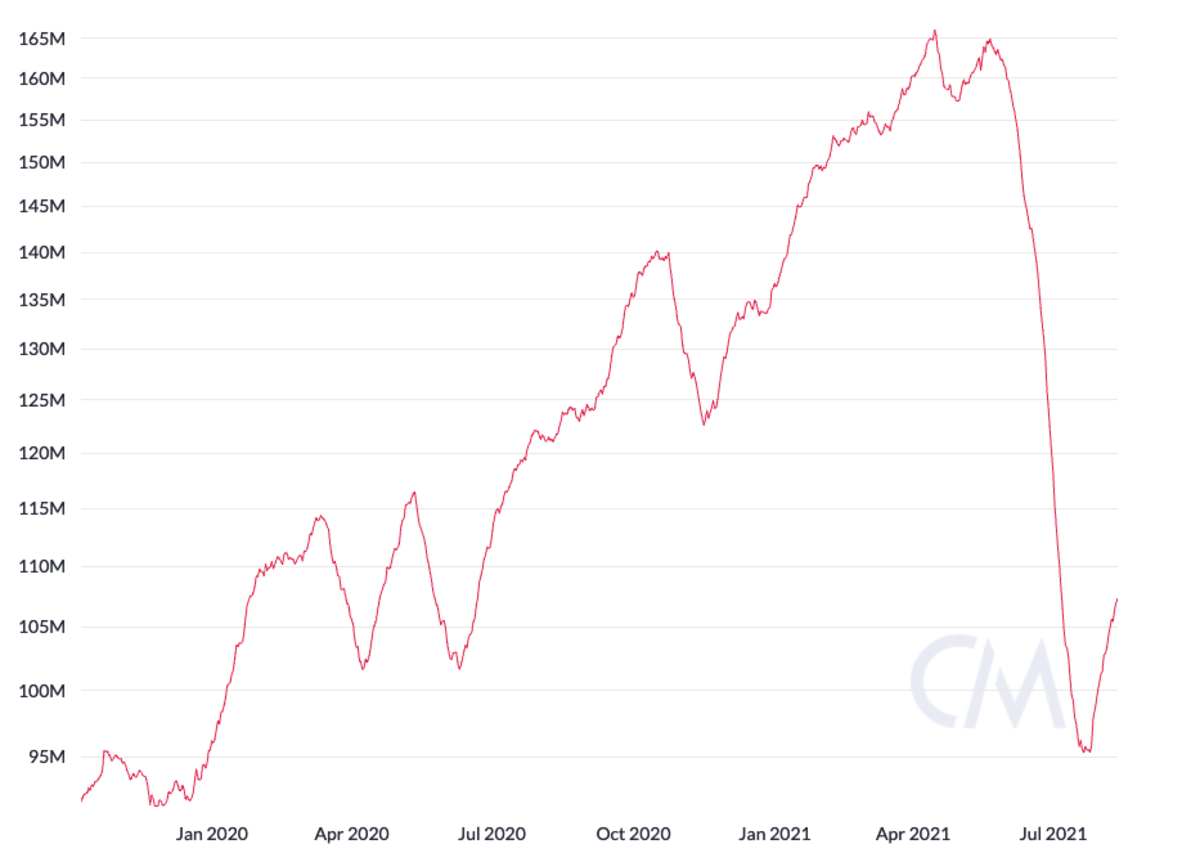

Ever since China started instituting a nationwide crackdown on bitcoin mining, the country has been losing its spot as the industry's hotbed. As companies were ordered to pull the plug and probed from maintaining operations in the country, the total Bitcoin hashrate started declining rapidly. But now, as miners are successfully finding a new home and rebooting operations, the hashrate has been trending up.

In May, China's state council recommended the country act on a renewed crackdown on bitcoin mining and trading, prompting local governments to target bitcoin miners with shutdown orders and inspection notices. What started as a crackdown on fossil fuel-powered plants developed to become a nationwide effort to ban bitcoin mining, triggering the great ASIC exodus.

In under 30 days, the Bitcoin network's total hashrate dropped by more than 40%, as miners shut down their operations and leave China on short notice. Miami, Florida, Russia, and El Salvador were some places that sought to attract Chinese miners and capitalize on the movement. Some opted for near Asian countries, however, with BIT Mining setting up shop in Kazakhstan. As a plus, the Bitcoin hashrate has been becoming even more decentralized.

Bitcoin implied daily hash rate, 30-day moving average, logarithmic scale. Source: CoinMetrics.

But hashrate has been recovering. As miners move their operations away from Chinese soil and get their rigs back online, more hashrate is employed on the Bitcoin network overall. Currently, the seven-day Bitcoin hashrate moving average is at 114 exahashes per second (EH/s) – higher than November 2020. And it can be reasonably expected to see hashrate keep trending up as more miners relocate successfully.

Hashrate recovering demonstrates that all facets of Bitcoin are indeed antifragile, governed purely by free-market principles. Ultimately, Bitcoin cannot be banned; it simply flocks elsewhere if one country chooses to go down that route. And that is true for mining and trading alike.